What are T-Bills?

T-bills, short for treasury bills, can be complicated to understand at first glance. However, once you deep-dive, T-bills are very straightforward to understand and easy to apply.

In simple terms, T-Bills are a type of Singapore Government Securities (SGS) that is very popular amongst investors in Singapore as a very safe form of investment when interest rates are high. They are fully backed by the Singapore Government and are considered almost (not totally!!) risk-free (if you hold it to term).

T-Bills are pretty popular as you can use cash, SRS, and CPF to invest in them. The downside of T-Bills is that you must hold them to maturity and you cannot redeem them early. You can, however, sell them in the secondary market.

T-Bills are considered short term investment and there are 2 types of holding period – 6 months and 1 year investment holding period. You can apply to invest in them every 2 weeks (for the 6 months bond) and every 3 months (for the 1 year bond).

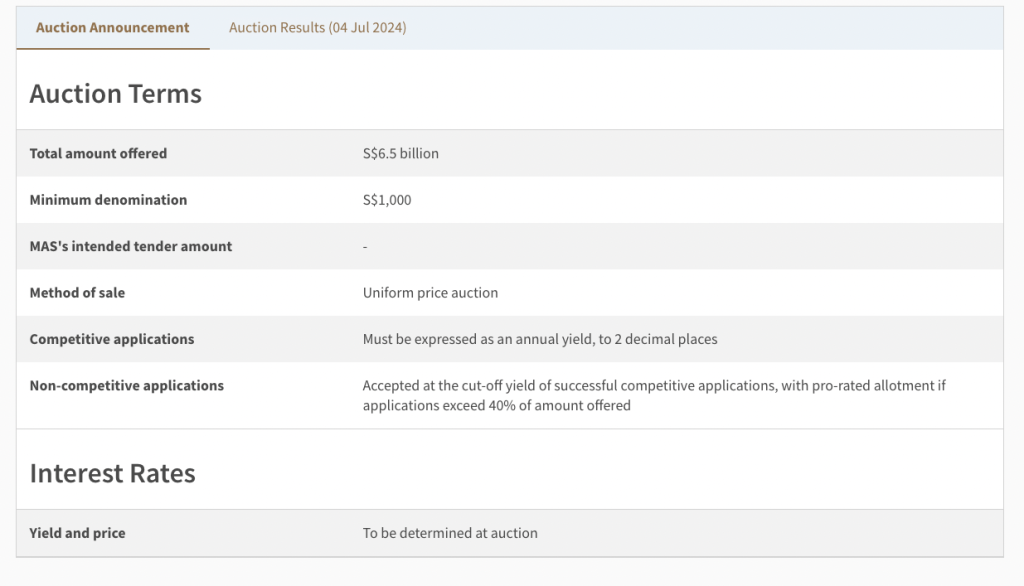

T-Bills have a relatively low entry barrier and the minimum investment starts from $1000, and subsequently $1000s increment. There is an investment limit of $1 million per applicant for non-competitive bids. There is also an allocation limit of 15% in total for every auction per individual.

How T-Bills work?

The TL;DR of T-Bills is:

- You invest $10k into a 6 months T-Bill at 3% interest rate

- You will receive $150 (interest) if your investment is successful

- You will receive the full investment ($10k) 6 months later

You buy the T-Bill at a discounted rate (you will receive a refund of your interest at the start) and receive the full amount upon redemption (once investment completed).

Types of T-Bills

There are 2 types of T-Bills – competitive and non-competitive bids.

Non-Competitive Bids

Non-competitive bids are the easiest to understand and the ones that most people will opt for. To apply for non-competitive bids, you simply need to indicate the amount you like to invest. You will know the interest rate and the amount you are allocated after the auction results is announced.

You can go for non-competitive bids if you do not care what the interest rates are, or simply do not know what yield to bid for. If the demand is high, it is highly likely that you will not be allocated the full amount that you want.

Competitive Bids

Competitive bids are slightly harder to understand. You can go for competitive bids if you only want to invest if the interest is above a certain interest. You will need to indicate the amount you like to invest, and what kind of yield you will accept for your investment.

For example, you want to invest if the interest rate given is 4%. You will then indicate the amount you want to invest along with the interest that you want. Once application is closed, they will start to allocate from the lowest interest rate placed to the highest, until the full amount offered is allocated.

Can you apply for T-Bills?

As long as you are at least 18 years old, anyone can apply for T-Bills. This includes Singaporeans, Permanent Residents (PR), and non-residents.

What is the interest rate for T-Bills?

T-Bills does not announce their interest rate prior to the application. Instead, they are determined based on the cut-off yield from the competitive bids.

You can check the official MAS website for the auction results and find out the interest rate there.

How do you buy (apply) T-Bills?

It is relatively easy to buy (apply) for T-Bills. However, note that application for T-Bills is not amendable or revocable, so think carefully before applying for them.

There are 3 methods to buy T-Bills – cash, Supplementary Retirement Scheme (SRS), or CPF Investment Scheme (CPFIS).

Method 1 – Cash

If you are using cash, follow the step-by-step guide below to buy T-Bills.

Step 1: Sign up for a Central Depository (CDP) account

You will need a Central Depository (CDP) account with Direct Crediting Service (DCS) before you can apply for T-Bills. You can open a Central Depository (CDP) account online via the SGX website.

Step 2: Open a local bank account (DBS/POSB, OCBC and UOB)

You will need a local bank account, namely DBS/POSB, OCBC, and UOB to apply for T-Bills. You can either open a bank account online (DBS/POSB, OCBC, and UOB) or via walk-in to any of the branches around Singapore.

Step 3: Apply via ATMs or Internet Banking (IB)

Once you have both accounts ready, you can apply for T-Bills either via any of the local bank ATMs or via Internet Banking (IB). You will need your CDP account number with you and ensure that the bank account is adequately financed by the amount you intend to invest.

Step 4: Wait for the allotment result

You can check the application results via the MAS website. You may be allocated less than what you applied for if there is a high demand for T-Bills for that particular month.

Step 5: Enjoy the interest payment

Once your application is successful, you will receive the interest from your investment on the issue date. The interest is automatically credited to the bank account that you linked to your Central Depository (CDP) account.

Method 2 – CPF Investment Scheme (CPFIS)

Step 1: Sign up for a CPF Investment Account

If you are buying T-Bills with your OA account, you will need to create a CPF Investment Account with the 3 local banks.

If you are investing with your SA account, no creation of CPF Investment Account is required.

Step 2: Apply via various portals

There are different application methods depending on the account (OA/SA) and the bank (UOB/OCBC/DBS) being used.

A quick summary:

For OA

- DBS/POSB: Apply through DBS/POSB’s internet banking portal.

- OCBC: Apply through OCBC’s internet banking portal or OCBC Digital application.

- UOB: Apply for SGS bonds in person at any UOB branch. Apply for T-bills through UOB’s internet banking portal.

For SA

- DBS/POSB: Apply in person at any DBS/POSB branch.

- OCBC: Apply through OCBC’s internet banking portal or OCBC Digital application.

- UOB: Apply in person at any UOB branch.

Ensure that the respective account is adequately financed by the amount you intend to invest. Note that banks charge some fees for the purchase of T-Bills using CPF OA.

Step 3: Wait for the allotment result

You can check the application results via the MAS website. You may be allocated less than what you applied for if there is a high demand for T-Bills for that particular month.

Step 4: Enjoy the interest payment

Once your application is successful, you will receive the interest from your investment on the issue date. The interest is automatically credited to the account that you apply from.

Method 3 – Supplementary Retirement Scheme (SRS)

Step 1: Sign up for a Supplementary Retirement Scheme (SRS) account

You will need a Supplementary Retirement Scheme (SRS) account to apply for T-Bills. You can open a Supplementary Retirement Scheme (SRS) account by walking into any branch of the 3 local banks.

Step 2: Apply via Internet Banking (IB)

Once you have your Supplementary Retirement Scheme (SRS) account ready, you can use the Internet Banking (IB) of your chosen bank to apply for T-Bills.

Ensure that the Supplementary Retirement Scheme (SRS) account is adequately financed by the amount you intend to invest.

Step 3: Wait for the allotment result

You can check the application results via the MAS website. You may be allocated less than what you applied for if there is a high demand for T-Bills for that particular month.

Step 4: Enjoy the interest payment

Once your application is successful, you will receive the interest from your investment on the issue date. The interest is automatically credited to the Supplementary Retirement Scheme (SRS) account.

How do you sell (redeem) T-Bills?

You cannot redeem T-Bills before it matures.

You can, however, sell them in the secondary market through any of the local banks by visiting their branches. The prices will fluctuate based on market conditions and you may or may not sell them at a gain or loss.

A quick glance at your investment

Let’s take a look at how much returns you will get if you invest with T-Bills.

Details

If you are starting out with T-Bills, this is a quick walkthrough on understanding the basic information of the current issue.

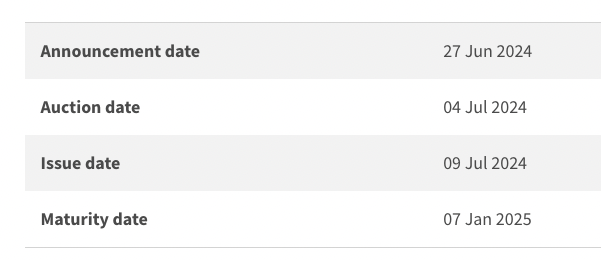

We will use the 27 Jun issue (BS24113N) in this case.

Let’s take a quick look at the MAS website for details on the current T-Bill issue. You would have known the timeline of the upcoming issues as they follow a schedule.

When the issue is announced, it also marks the start of application. Application will close 1 business day before auction.

Again, note that the interest rate is not announced as they are determined after auction have closed.

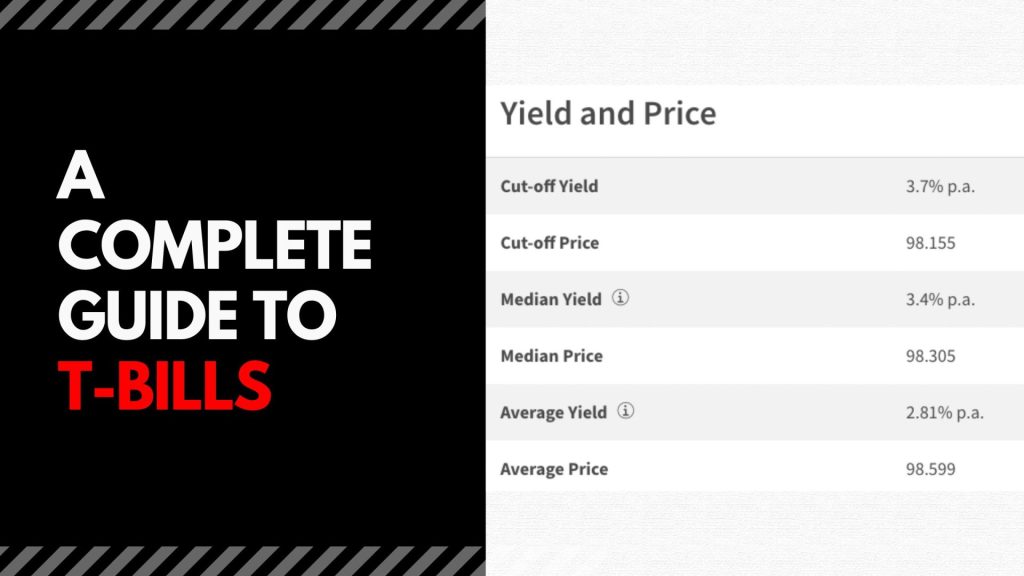

You can have an inkling of the expected interest rate by reviewing the past statistics of T-Bills. The column to look at to know about the past yield is “Cut-off Yield (%)”.

You will be receiving the interest on the issue date, and the principal sum that you invested after the investment have matured.

Interest Illustration

Assuming you are investing $10,000 with 6 months T-Bill, and it is announced that the interest rate for the issue is 3.5%, you will receive $175 at the end of the investment.

interest = (10,000 x 3.5%) / 2 = $175

How do you check your existing T-Bills investment?

You can easily check your existing T-Bill investment using the CDP portal offered by MAS if you purchase them in cash and the SRS/CPF portal if you purchase them in SRS/CPF funds.

Should you invest in T-Bills?

T-Bills should be treated like an investment product, and before investing in them, you need to know your risk appetite and your desired financial portfolio.

Pros – Short Investment Horizon

T-Bills have a very short investment period of 6 months or 1 year. This makes it easier for investors to hold till maturity. They are also great for investors that would not need the money for the next few months, and is looking for short-term investments to park their money in.

If you are expecting to spend a certain amount of money at a specific time (eg, wedding, car, house), they are also great for you to “lock” your money while getting your interest upfront to spend on.

Pros – Low Capital Required

One of the selling points of T-Bills is that it does not require a high capital to invest. In fact, the minimal investment amount required is $1000 to a maximum of $1 million, in multiples of $1000.

If you are a beginner investor or are looking to slowly build up your portfolio, T-Bills are ideal to get started as the entry to get started is relatively low.

Pros – Very Low Risk

As mentioned previously, the T-Bills are fully backed by the Singapore Government and have a AAA credit rating. This means that there is a very low risk of default and T-Bills are generally one of the safest assets to invest in Singapore.

Cons – Reinvestment Risk

T-Bills are very short term investment of either 6 months or 1 year. Once your investment matures, you will have to source for other investment. By then, the investment landscape may have changed, and you would not be able to get similar interest rates.

Cons – Illiquid Investment

If you are someone who needs their money to be easy to access, T-Bills are not for you. Once you commit to the investment, you cannot redeem it early. While you can sell them in the secondary market, there is a chance you may sell them at a loss or gain.

Cons – Unpredictable Interest Rate

While there is always the historical rates that we can fall back on to predict the interest rate (yield) for the upcoming T-Bill issue, there could always be a black swan event (such as Covid) that will greatly swing the market. You may or may not end up with a worse-than-expected interest rate when such situation happens.

T-Bills Hack

If you are an existing investor of T-Bills or are looking to invest in T-Bills, these are some tips to maximize your use with T-Bills.

Hack #1 – To Get Full Allocation

T-Bills can get notorious popular when interest rates are high. It could be oversubscribed and you might not be able to get the full allocation you want.

One thing you can do is to apply for competitive bid and enter an interest rate that is significantly lower than the expected interest rate (check past interest rate for performance). You should be able to get the full allocation as competitive bid will be allocated starting from the lowest bid.

Hack #2 – Get Monthly Income (Dividend) Using The T-Bill Ladder Hack

It is usually not wise to put all your money in one basket. T-Bills will not announce their interest rate before application. Rather, the interest rate is determined based on the auction results whereby it is the highest accepted interest rate of successful competitive applications and announced after.

By splitting your money, preferably in 6 different issues, you would be able to diversify your risk, and you would also be getting passive income every month. Every time an issue matures, you can then use the capital to put in the next issue and repeat the cycle.

Last Updated: 01 Jan 2025