One year after UOB revised the interest rate of its UOB One account, OCBC is finally revising its interest rate, which will be effective in May 2025. While this is a long-expected move, it does not make the news easier to digest. The change in the interest rate is rather drastic, and the drop in interest rates is very stark.

A quick summary below.

Interest Before 1 May 2025

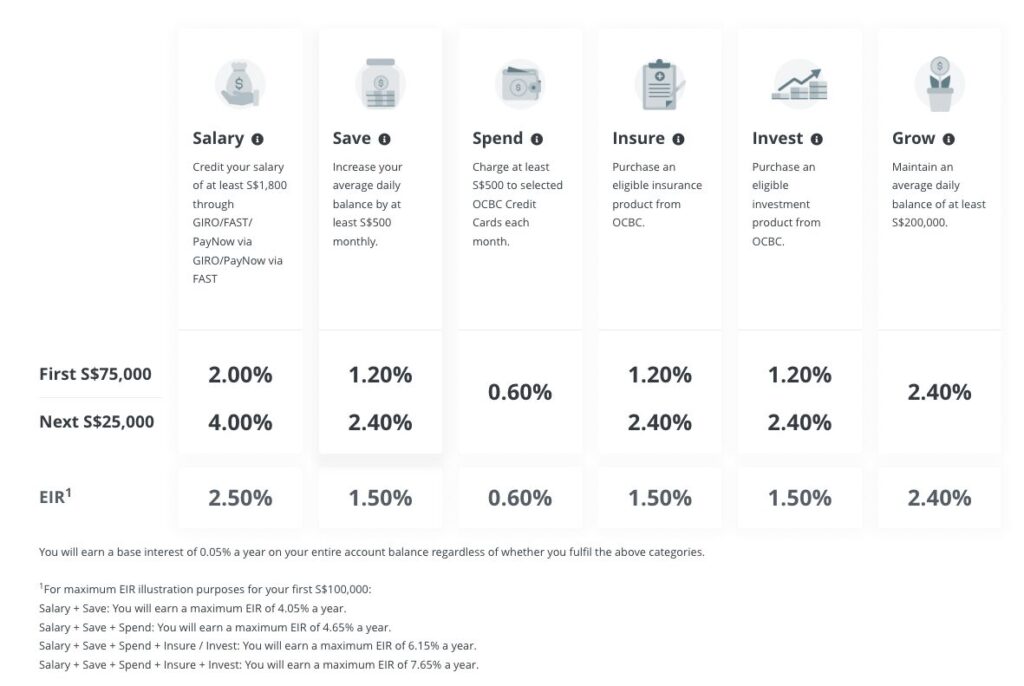

In the good days before May 2025, the maximum effective interest rate (EIR) you can receive is 7.65% if you do salary + save + spend + insure + invest with OCBC. The easy criteria to hit are salary + save + spend, which will also give a good interest rate of 4.65% a year. The bare minimum of crediting your salary with OCBC also give a good rate of 2.55%. This is almost equivalent to many FD interest rates nowadays.

These interest rates are calculated on the first $100k of your account balance and you also get a bonus of 2.4% on the first $100k if you have $200k in balance with OCBC. These were great when all other banks were adjusting their interest lower and interest rates of SSB is falling below 3%.

Interest From 1 May 2025

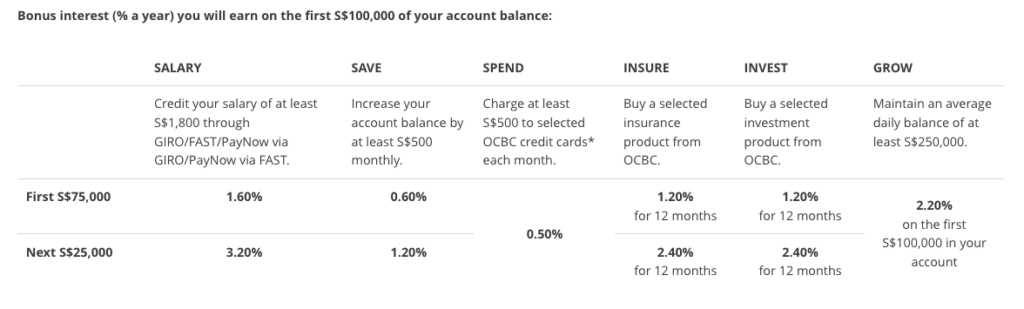

The maximum effective interest rate (EIR) you can receive is now 6.3% if you do salary + save + spend + insure + invest with OCBC. If you meet the easier criteria of salary + save + spend, you will get 3.3%. If the most basic criteria of crediting your salary are met, you can get 2.05% in interest.

These interest rates are calculated on the first $100k of your account balance. There is a bonus of 2.2% on the first 100k balance, only if you have 250k in your account. This is an increase of 50k in savings required to be deposited in the OCBC 360 account, and it is definitely a significant drop in interest.

The only interest rate that remains constant is the insure + invest category which, let’s be honest, not a lot of people are going to be able to hit. Overall, the drop in interest rate is very significant, and it would be a tough decision whether to continue with OCBC 360 account, given that interest rates everywhere are equally depressing as well.

Should You Still Use OCBC 360 Account?

OCBC 360 Account is a very straightforward account with an easy-to-use online banking interface, and it is a local bank name that many trust and use. While the adjustment is pretty drastic, it is in line with the overall macro environment where interest rates have been dropping for the past few months.

The overall requirements are the same, and you do not need to adjust your spending or financial decisions to meet the criteria to get the higher interest. One particular change, however, is you would need to maintain a higher balance of $250k in your OCBC 360 account to be able to get the higher interest from the grow component.

This means that instead of receiving $2400 per annum on a 200k balance, you are only receiving $2200 per annum on a 250k balance. This means the effective interest rate have dropped from 2.4% to 1.76%. This is definitely a turn-off for larger accounts who are looking for a place to stash their extra cash.

OCBC 360 is the only high-interest savings account out of the 3 local banks that allows you to get higher interest with just salary crediting. DBS and UOB require an additional category, such as spending on their credit cards to get a higher interest rate. With this salary crediting, you can get 2.05% effective interest rate on the first $100k of the account balance.

If you are spending on debit/credit cards on top of crediting your salary, OCBC 360 gives an effective interest rate of 2.55% on the first $100k of the account balance. UOB One gives an effective rate of 4% on the first $150k of the account balance. DBS Multiplier gives an effective rate of up to 2.2% on the first $50k of the account balance.

With a minimum spending of $500 on cards and a minimum salary crediting of $1600, UOB gives the highest interest of 4% pa among the 3 local banks. In addition, the interest is given on a higher base amount of $150k, which will give you a neat $500 in monthly interest.

You can also get a slightly lower interest of 2.4% on the first $125k in UOB if you have 3 GIRO transactions instead of salary crediting. Check out our article on the new UOB One interest rate here! UOB last changed the interest rate of UOB One account in May 2024. There could be a real possibility that UOB will also adjust its interest rate soon, following the adjustments by OCBC.

The great thing about OCBC is that there is also a save category, where if you increase your account balance by $500 monthly, you will also get an additional 0.75% interest, which helps to bring up your effective interest for salary crediting only to 2.8% and salary crediting + $500 credit card spending to 3.3%. This is probably the easiest criterion to hit for OCBC for typical people.

After analysis, it seems the best way to optimize the new interest rate revision is to focus on UOB and hit $500 card spending + salary crediting to get 4% interest rate. Whatever remaining should be credited to OCBC to get 1.3% if you increase your account balance by $500 monthly + spend $500 CC. Of course, it is also probably to seek out better options such as SSB or T-Bills instead of earning such a low interest rate.

Last Words

High-interest savings accounts (HYSA) seems to lose their appeal to many given that rates have been falling due to market conditions. However, as a single income family, having fall-back money that we can access easily is important to us, especially during rainy days. Hence, we will continue to use HYSA to store our emergency money even as banks review their rates.

Last Updated: 29 Mar 2025