We expected other banks to follow OCBC’s footsteps in lowering their interest rates for their high-yield savings account (HYSA). However, we did not expect this move to be so soon. UOB dropped the interest rate for their UOB One account one week after OCBC made the news, and it is equally as painful to read. The bummer — the new rates from OCBC and UOB will both kick in from 01 May 2025.

Interestingly, UOB also adjusted their interest rates exactly one year before!

Read on for a summary of the interest rate.

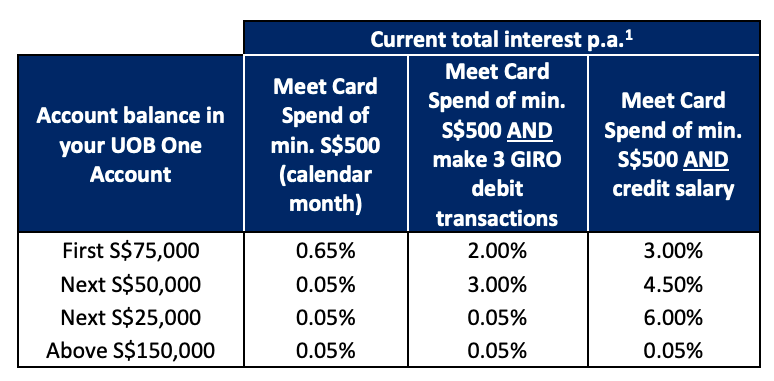

Interest Before 1 May 2025

Right now, UOB One account holders are enjoying up to 4% interest rate if you have $500 credit card spending + salary crediting. If you have $500 credit card spending + 3 GIRO transactions, you can get an effective interest rate of 2.4%. At the most basic, $500 credit card spending will give you 0.65%.

These interest rates are applicable on the first $150k of your UOB One balance if you take the “salary crediting” path and the first $125k if you take the “3 GIRO transactions” path.

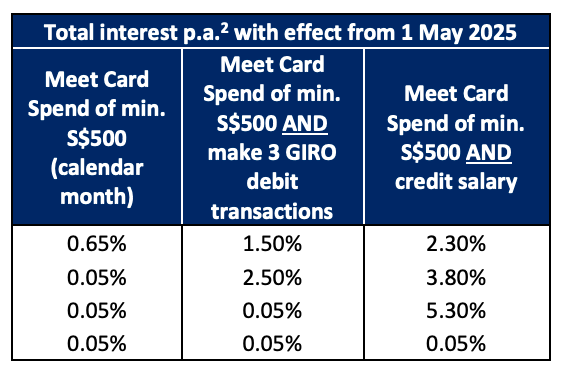

Interest From 1 May 2025

Moving on, the highest effective interest rate you can get from $500 credit card spending and salary crediting is 3.3% for the first $150k of the account balance. The highest effective interest rate for $500 credit card spending + 3 GIRO transactions is 1.9% for the first $125k of the account balance.

At the most basic, $500 credit card spending will give you 0.65%, which remain the same as the previous interest rate.

UOB One is also keeping the criteria to hit the higher interest rates the same, so you do not have to do anything. The bonus interest you have been receiving monthly will just be dropped quite significantly.

Should You Still Use UOB One Account?

After all the adjustments, UOB One and OCBC 360 have now both similar interest rates for salary crediting + spending $500 on credit cards at 3.3%. The main difference is, the interest is over first $150k balance for UOB and $100k for OCBC. This would give you an extra $1650 annually if you choose UOB.

In addition, for you to earn the higher interest of 3.3% in OCBC, you would also need to ensure that your account balance is also increasing by $500 monthly. This is slightly annoying as you would need to keep track of the account balance.

One key thing to note is OCBC only consider giving the higher interest for salary crediting if you are crediting at least $1800 and UOB requires you crediting at least $1600. So do make sure to check the minimum salary criteria as well.

If you are a small spender, you may find it hard to get the higher interest rate in UOB One Account as they prioritize card spending criteria achieved before they check for salary crediting/3 GIRO transactions. If you so happens to not hit $500 credit card spending, you will not get the higher interest. The same situation for OCBC, you will still get 2.05% for just crediting salary.

UOB One Account is also great for people who does not have salary, but have lots of bills. They are the only bank so far, that gives a bonus for making GIRO transactions with them. However, the effective interest rate you are receiving is 1.9%.

Our Gameplan

Right now, looking at the ways things are going, we will move our salary crediting from OCBC to UOB to get the higher interest of 3.3% over an account balance of $150k. We will be able to get $4950 annually with UOB One Account.

Whatever remaining will be kept in OCBC 360 to earn 1.3% if we increase the account balance by $500 and spend $500 on credit cards. This is a temporary setup while we assess what other form of investments we would want to take on instead. Based on the current trend, SSB and T-Bills will also take a hit and we would not be surprised if interest rates fall below 2.5%.

If you guys have any investments, do suggest to us!

Last Updated: 02 Apr 2025