Mortgage loan is the only debt that we have since we paid off our student loans many years back. We are, in a way lucky, that we do not have other loans as we live within our means. We do not have a car, so we do not have any car loans. Our renovation for our apartment is kept minimal since we brought an Executive Condo (EC) where most of the furnishing is ready. We also do not have any credit card debt since we are careful about keeping within budget.

Since we only have this single debt, we are very conscious to have some savings in the back of our pocket, ready to make partial payments when the interest rates are high. This is the exact situation we were in more than 2 years ago, when the fixed rate of our mortgage loan more than doubled to 4.x% from 1.x%. After much discussion, we began our journey of making active partial payments whenever we had some spare cash or when our fixed deposits (FDs) matured.

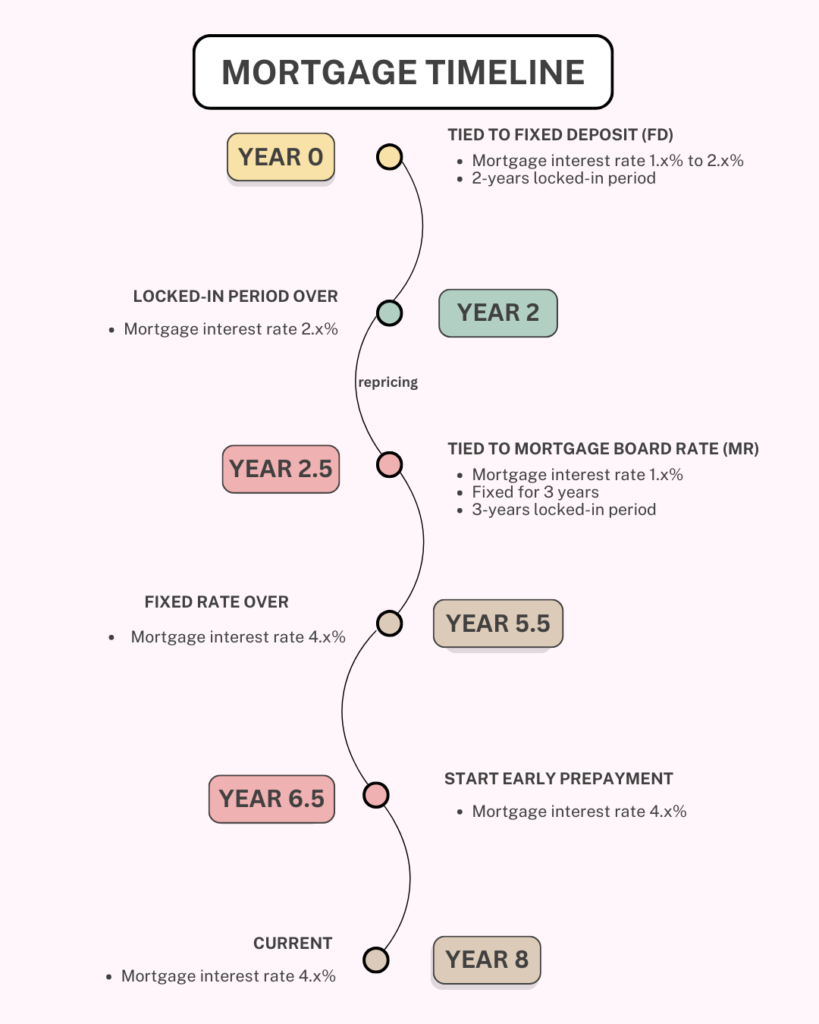

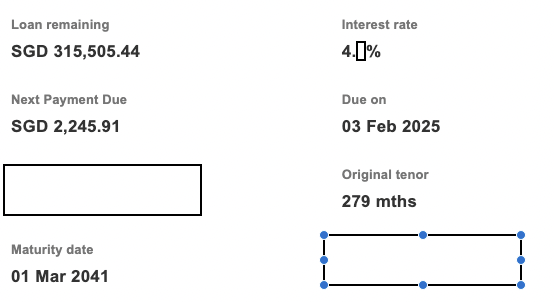

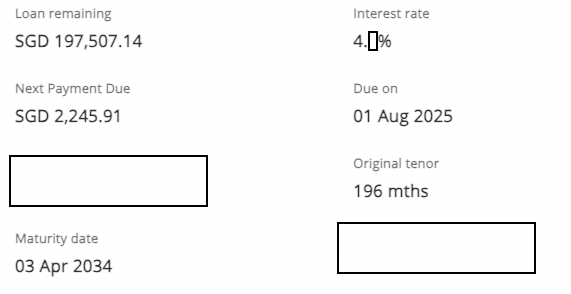

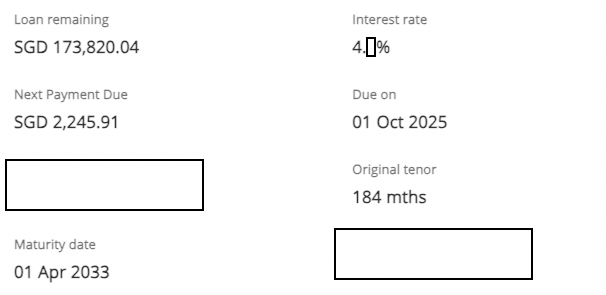

Mortgage Rates Timeline

We started with a mortgage package tied to the Fixed Deposit (FD), with a 2-year lock-in period. Mortgage interest during this period was 1.x% to 2.x%. Once the 2-year lock-in period ended, the mortgage interest remained at over 2%.

We started shopping for potential repricing/refinancing candidates. Then Covid hits, and it was a period of low mortgage interest rates.

We took the opportunity to reprice to another package – a fixed mortgage package with 3-year fixed rate and a 3-year lock-in period, tied to the Mortgage Board Rate (MR)(on hindsight, this was a bad move). Mortgage interest went down to 1.x% during these 3 years.

Once the 3-year fixed rate is up, our mortgage interest rate more than doubled to 4.x%. Unfortunately, global inflation and FED rate hikes pushed all mortgage interest rates in Singapore high. It didn’t make sense to refinance or reprice, as the alternative options have similar interest rates to our current package.

That was 2.5 years ago. After more than 1 year of waiting, mortgage interest rates started to drop across Singapore to 2.x%. Instead of refinancing or repricing, we decided to start our partial payment towards our mortgage loan. We covered the main reasons why we do so here.

We have been making partial payments for the past 15 months. However, we have decided to pause the early prepayments as we have a major change in our lives.

A visual chart of our mortgage timeline is below.

Why did we not refinance/reprice now that interest rates are low?

We did consider refinancing or repricing, but after considering a few factors, we decided to hold off the thought and redirect our focus on making partial payments whenever financially possible.

We outline our thoughts in this article. You can read about our rationale here.

Progress Chart

We are pretty happy with how things are progressing. In fact, we have paid off more than 50% of our remaining mortgage loan via partial payment in the last 15 months. This is to us – is an amazing feat – given that we transitioned to a single-income family more than 3 years ago and we have a toddler to splurge on.

The big reveal –

3 months in with $80k prepayment completed.

6 months in with $140k prepayment completed.

12 months in with $220k prepayment completed.

15 months in with $240k prepayment completed.

How much did we save in interest?

As we are constantly making prepayment every few months, it is hard to calculate the exact interest saved. Based on a rudimentary calculation, it is expected that the estimated savings from our efforts is $202k.

Assuming our interest rate remains constant till the end of the loan period at 4.x%, we have an estimated 23.5 years of loan tenure remaining. If we were to stick to this timeline, the estimated mortgage interest that we have to pay over the next 23.5 years is $245k.

Over the course of 15 months of doing early prepayment, we have paid an estimated $14k in interest. Assuming we are not doing any prepayment, we will be left with approximately 7.5 years of the loan. The estimated mortgage interest for the next 7.5 years is $29k. This means our total interest paid would be $43k.

Why do we choose to shorten the loan tenure VS reduce the installment amount?

Initially, we were to reduce the installment amount. This would allow us more cash flow and give us more time to pay off the loan. However, after calculating the interest saved, we decided to shorten the loan tenure as it saved us a lot more interest instead.

As a quick illustration,

If you have a $500k loan, with an interest of 4%, and a 20-year loan tenure, the interest you would be paying is $227k. You decide to make a prepayment of $1k a month on top of your monthly installments.

If you opt to keep the installment amount the same, and reduce the loan tenure instead, you will pay $146k in interest and bring forward your payment schedule by more than 6.5 years.

If you opt to reduce the installment amount instead, you will pay $175k in interest and bring forward your payment schedule by around 1.5 years.

What if we invest the funds instead?

We made a total prepayment of $240k. Since we have the funds, what if we had invested in it instead?

At a return of 3% compounded, we would have a total return of $241k by the end of 23.5 years.

At a return of 4% compounded, we would have a total return of $363k by the end of 23.5 years.

At a return of 5% compounded, we would have a total return of $515k by the end of 23.5 years.

At a return of 6% compounded, we would have a total return of $703k by the end of 23.5 years.

At a return of 7% compounded, we would have a total return of $937k by the end of 23.5 years.

Sounds really great isn’t it?

The power of compounding is very strong. And if time were to turn back, we might have invested the funds instead. However, investing does not always translate to returns. It requires a lot of discipline and knowledge that we are trying to learn and build. Now that we are trying to build a long-term portfolio, it is painfully obvious that investing is a test of patience.

Like all humans, we have emotions. If we see gains, we tend to sell to realise the gains. If we see loss, we also tend to sell to prevent more loss. Returns are also not linear, and seeing ups and downs in your portfolio is also a test of patience and discipline.

At the end of the day, the choice is made, and we cannot reverse the decision. Regardless, we believe that clearing debts is a good use of our money, and having that stability really comes in handy now (read below why).

Future Plans

Initially, we had given ourselves 5 years to clear the loan as much as we can (or even fully pay off the loan!!), and we ended up with quite a bit of leeway. However, we do expect that the progress would drastically slow down as the working parent is expected to be retrenched(!!) in the upcoming company layoff.

We will be moving to a defensive stance and are conserving all our cash while thinking of our next move. In a way, we are really glad that we made consistent efforts in the past to reduce our debts. Now, we are not as stressed about the potential layoff. Having a reduced debt makes potential job search less stressful as we are not “forced” to take on roles we do not like, “just for the money”.

Once everything is settled and one of us eventually finds a job, we do see ourselves continuing the prepayment. It simply makes more sense to continue the effort, as it helps us mentally not to be worried about money. It also gives us the option to take a break from working if the environment is toxic, and allows us to live more freely without having debt constantly as a shadow.

Last Updated: 22 Sep 2025