Singapore Saving Bonds (SSB) is a government-backed, almost risk-free investment. It is considered a safe investment and is extremely popular amongst risk-averse investors as you can get back your investment in full with no penalty should you decide to withdraw. You can check out our guide here for more information on Singapore Saving Bonds (SSB)!

The TL;DR of Singapore Saving Bonds (SSB) is that it is a 10-year bond that has a pre-determined interest rate. Interest on your investment is given bi-yearly and the longer you hold it, the higher the interest.

Every start of the month, we would always check the official Singapore Saving Bonds (SSB) website to check the announced interest rates, and consider if it is worth it to park our money with them.

SSB Interest Rates

The interest rates of Singapore Saving Bonds (SSB) vary and we have seen some really good interest rates offered by SSB in 2023.

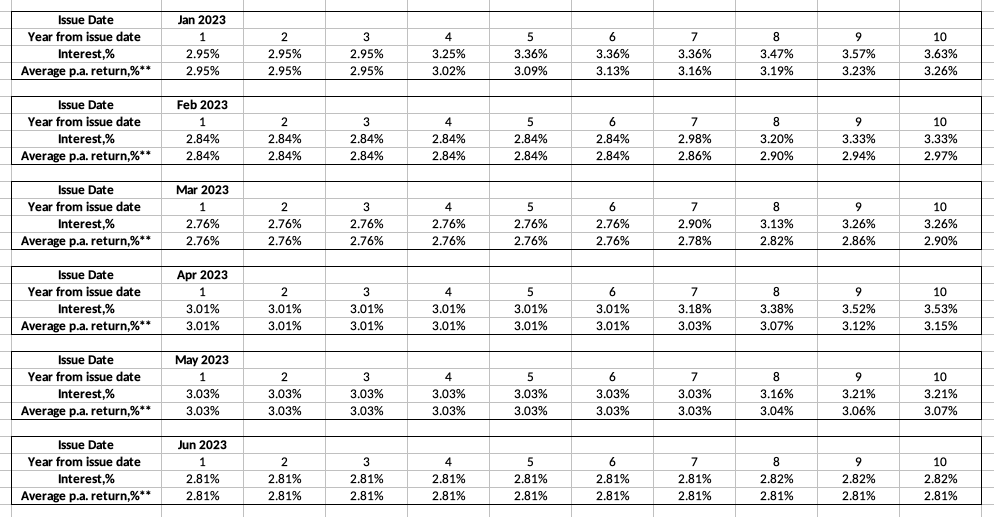

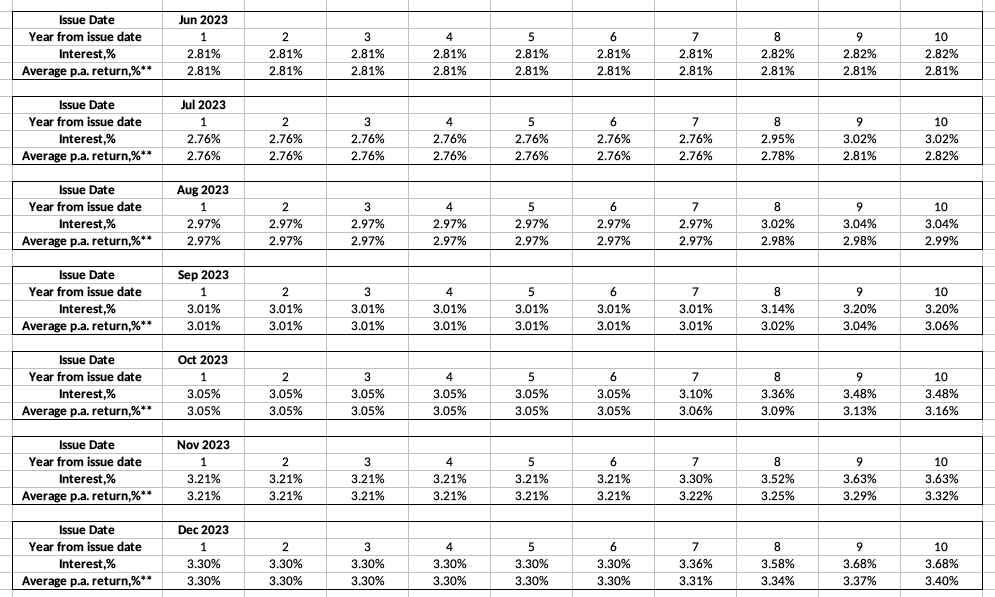

2023 interest rates

The interest offered by SSB in 2023 is so good, that many issues were oversubscribed. At one point, the highest interest offered is during the Dec 2023 issue at 3.4%. This beats a lot of fixed deposit offerings out there and there was a lot of attention shifting back to SSB.

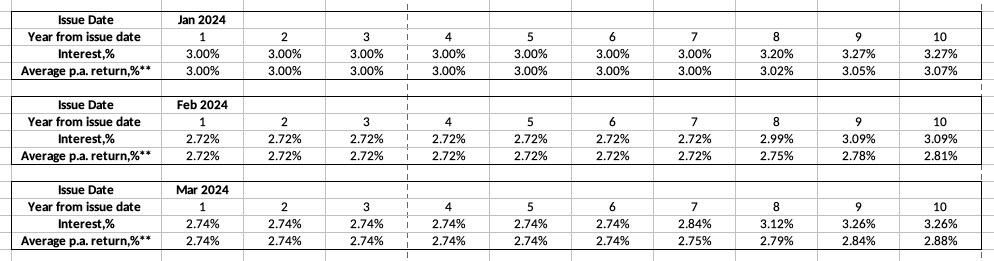

2024 interest rates

In 2024 however, we can see a notable drop in the interest rates offered, with the interest rate for the most recent 2 issues dipping to below 3%. We observed that the demand and interest for SSB also started to fade with the recent issues being undersubscribed.

Our future forecast

Based on the current interest environment, it is likely that we are looking at a further decrease or relatively stagnant interest rates. It is unlikely that we will see high interest rates for SSB for a couple of months.

Should you still put your money in SSB?

Many investors are probably wondering if it is still a good idea to put their money in SSB. Here’s what we think.

Better options with higher returns

Understand different other options on how to make your money work harder. Are you able to put the investment to better use and get higher returns in another financial instrument such as stocks, bonds, or even options? If you can make your money work for you in other avenues, SSB may not be as appealing.

Just a quick check on Fixed Deposits (FD) in local banks can yield you more than 3% of interest! Explore your options, and weigh the returns and risks before deciding if SSB is the right place for you to put your money.

Investment timeframe

Before every investment decision, assess if there is any timeframe in which you need the money. SSB has a 10-year investment period that makes it a good instrument for long-term investment. While it is possible to withdraw it anytime within the 10-year investment, SSB employs a step-up interest approach whereby the interest is higher the longer you hold it.

In any investment portfolio, cash is an important component, but many fail to recognize its purpose. SSB is ideal for cash components that you have no immediate purpose for, and are willing to hold for long term.

Access to funds

While it is relatively easy to place a request to withdraw the funds from SSB, the funds will only be released to you at the start of the following month. If these funds have been earmarked for immediate use or emergency, it may not be ideal to park them in SSB as you do not have the fluidity of accessing these money every time there is an emergency.

Risk appetite

SSB appeals to investors who are generally more risk-averse or are looking to balance their portfolio with low-risk financial instruments. So long as the interest rates offered by SSB are higher than the base 0.05% interest rate that most banks offer for their savings account, it could still be considered as a safe haven to earn a better interest rate while waiting for the next opportunity.

Last words

Apart from SSB, the other most common low-risk financial instrument tools are fixed deposits (FD) and high-interest accounts. Of course, many of these financial instrument tools move in tandem and we observe interest rates falling across the board. Regardless, these are great alternatives for SSB if you would like to weigh in on your options.

SSB is almost a no-brainer, low-effort, and almost risk-free investment. They can be great for investing beginners and risk-adverse investors, alongside seasoned investors looking to balance their portfolios. At the end of the day, we have different financial situations and it is important to consider every aspect before making any financial decision.

Last Updated: 02 Mar 2024