What are Singapore Savings Bonds (SSB)?

Simply put, Singapore Saving Bonds (SSB) is a type of Singapore Government Securities (SGS) that is suitable for individual investors like us to invest. SSB is fully backed by the Singapore Government, which means you can get your capital back in full with no capital loss. Due to this reason, most people consider investing in SSB to be very low risk.

Singapore Saving Bonds (SSB) have an investment period of 10 years, but the investments are not locked. This means that you can choose to exit your investment at any time during the 10 years. If you choose to withdraw your investment early, there is also no penalty or loss to your investment and you can get back your capital in full (along with some pro-rated interest).

Singapore Saving Bonds (SSB) have a relatively low entry barrier whereby you can invest with them if you have at least $500. The investment needs to be in multiples of $500 and the maximum investment you can go to is $200k.

The interest rates of Singapore Saving Bonds (SSB) take on a step-up approach where the longer you hold them, the higher the interest rate.

Can you apply for Singapore Savings Bonds (SSB)?

As long as you are at least 18 years old, anyone can apply for Singapore Savings Bonds (SSB). This includes Singaporeans, Permanent Residents (PR), and non-residents.

What is the interest rate for Singapore Savings Bonds (SSB)?

The application for Singapore Saving Bonds (SSB) opens at the start of the month and closes at the end of the month. Each application (issue) has different interest rates, and you can always check the rates on the official MAS website when they open for application.

How do you buy (apply) Singapore Savings Bonds (SSB)?

It is relatively easy to buy (apply) for Singapore Saving Bonds (SSB).

There are 2 methods to buy Singapore Saving Bonds (SSB) – cash or Supplementary Retirement Scheme (SRS). If you are using cash, follow the step-by-step guide below to buy Singapore Saving Bonds (SSB).

Method 1 – Cash

Step 1: Sign up for a Central Depository (CDP) account

You will need a Central Depository (CDP) account with Direct Crediting Service (DCS) before you can apply for Singapore Saving Bonds (SSB). You can open a Central Depository (CDP) account online via the SGX website.

Step 2: Open a local bank account (DBS/POSB, OCBC and UOB)

You will need a local bank account, namely DBS/POSB, OCBC, and UOB to apply for Singapore Saving Bonds (SSB). You can either open a bank account online (DBS/POSB, OCBC, and UOB) or via walk-in to any of the branches around Singapore.

Step 3: Apply via ATMs or Internet Banking (IB)

Once you have both accounts ready, you can apply for Singapore Saving Bonds (SSB) either via any of the local bank ATMs or via Internet Banking (IB). You will need your CDP account number with you and ensure that the bank account is adequately financed by the amount you intend to invest.

Note that there is a non-refundable transaction fee of $2 per application.

Step 4: Wait for the allotment result

You can check the application results via the MAS website. You may be allocated less than what you applied for if there is a high demand for Singapore Saving Bonds (SSB) for that particular month.

Step 5: Enjoy the bi-yearly interest payment

Once your application is successful, you will receive the interest from your investment every 6 months. The interest is automatically credited to the bank account that you linked to your Central Depository (CDP) account on the first business day of every month.

Method 2 – Supplementary Retirement Scheme

Step 1: Sign up for a Supplementary Retirement Scheme (SRS) account

You will need a Supplementary Retirement Scheme (SRS) account to apply for Singapore Saving Bonds (SSB). You can open a Supplementary Retirement Scheme (SRS) account by walking into any branch of the 3 local banks.

Step 2: Apply via Internet Banking (IB)

Once you have your Supplementary Retirement Scheme (SRS) account ready, you can use the Internet Banking (IB) of your chosen bank to apply for Singapore Saving Bonds (SSB).

Ensure that the Supplementary Retirement Scheme (SRS) account is adequately financed by the amount you intend to invest.

Note that there is a non-refundable transaction fee of $2 per application.

Step 3: Wait for the allotment result

You can check the application results via the MAS website. You may be allocated less than what you applied for if there is a high demand for Singapore Saving Bonds (SSB) for that particular month.

Step 4: Enjoy the bi-yearly interest payment

Once your application is successful, you will receive the interest from your investment every 6 months. The interest is automatically credited to the Supplementary Retirement Scheme (SRS) account on the first business day of every month.

How do you sell (redeem) Singapore Savings Bonds (SSB)?

There is a 10-year holding period for each investment. If you choose to hold it for the full 10 years, the capital along with the interest, will be credited to your bank account (for cash) or Supplementary Retirement Scheme (SRS) account (for SRS). No action is required from you and there are no transaction fees.

If you choose to sell (redeem) early, there are no penalty fees. There is, however, a $2 transaction fee for each request.

For those who have invested with Supplementary Retirement Scheme (SRS) account and wish to sell (redeem) early, you can log in to the Internet Banking (IB) offered by your chosen bank to submit a redemption request.

For those who have invested with cash and wish to sell (redeem) early, you can log in to Internet Banking (IB) or ATMs of any local banks to submit a redemption request.

There is a redemption deadline for each issue, you can check them at the official MAS website.

Once you have submitted your request, you will receive your capital (along with pro-rated interest) by the 2nd business day of the following month.

A quick glance at your investment

Let’s take a look at how much returns you will get if you invest with Singapore Savings Bonds (SSB).

Details

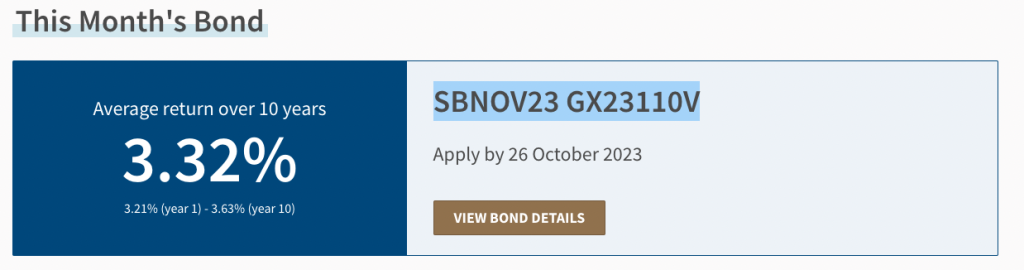

If you are starting out with Singapore Savings Bond, this is a quick walkthrough on understanding the basic information of the current issue.

We will use the Nov 2023 issue (SBNOV23 GX23110V) in this case.

Let’s take a quick look at the MAS website for details on the current Singapore Savings Bond (SSB) issue.

The interest you will be getting for this issue would be 3.32% on average, ranging from 3.21% to 3.63%.

You will be receiving the dividend payment every 6 months, which means you will be receiving the dividend every November and May.

The application timeline is provided. Do take note of the “closing date” of the application.

If you have existing Singapore Saving Bonds (SSB) that you wish to redeem, you can do so before the “closing date” as per the timeline below.

Interest Illustration

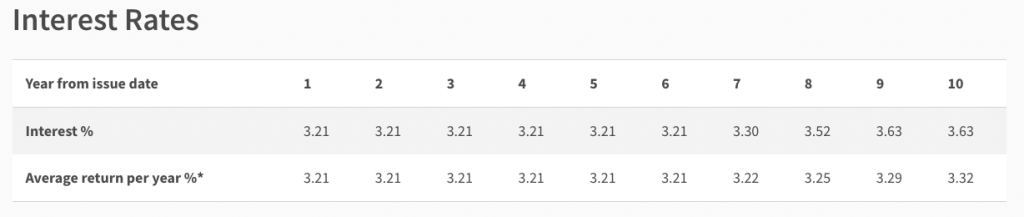

Assuming you are investing $10,000 with Singapore Savings Bonds (SSB), below is the expected interest you are likely to receive over the next 10 years.

| Year from Issue Date | Interest Rate (%) | Interest Received ($) |

| 1 | 3.21% | $321 |

| 2 | 3.21% | $321 |

| 3 | 3.21% | $321 |

| 4 | 3.21% | $321 |

| 5 | 3.21% | $321 |

| 6 | 3.21% | $321 |

| 7 | 3.30% | $330 |

| 8 | 3.52% | $352 |

| 9 | 3.63% | $363 |

| 10 | 3.63% | $363 |

If you hold the investment for the full 10 years, you would be able to receive $3334 in dividends in total over the 10 years.

You can also use the official Singapore Savings Bonds (SSB) calculator to calculate your projected interest.

How do you check your existing Singapore Savings Bonds (SSB) investment?

You can easily check your current Singapore Savings Bonds (SSB) investment using the SSB portal offered by MAS.

Should you invest in Singapore Savings Bonds (SSB)?

Singapore Savings Bonds (SSB) should be treated like an investment product, and before investing in them, you need to know your risk appetite and your desired financial portfolio.

Pros – Very Low Risk

As mentioned previously, the Singapore Savings Bonds (SSB) is fully backed by the Singapore Government. This means that there is a very low risk of default and Singapore Savings Bonds (SSB) is generally one of the safest assets to invest in Singapore.

Pros – Low Capital Required

One of the selling points of Singapore Savings Bonds (SSB) is that it does not require a high capital to invest. In fact, the minimal investment amount required is $500 to a maximum of $200k, in multiples of $500.

If you are a beginner investor or are looking to slowly build up your portfolio, Singapore Savings Bonds (SSB) are ideal to get started as the entry to get started is relatively low.

Pros – Easy To Buy/Sell

Another reason why Singapore Savings Bonds (SSB) is appealing is that the process of buying and selling them is relatively easy. You can buy or sell Singapore Savings Bonds (SSB) online without the hassle of visiting any bank branches. In addition, the interface to buy or sell Singapore Savings Bonds (SSB) is very clean and straightforward, which makes it easy for non tech-savvy people to buy or sell.

Cons – Not For High-Risk Appetite

If you are an investor with a very high-risk appetite, Singapore Savings Bonds (SSB) is probably not for you. Instead, Singapore Savings Bonds (SSB) is a very low-risk, low returns investment instrument and is widely used as a comparison with Fixed Deposits (FD).

Singapore Savings Bonds (SSB) Hack

If you are an existing investor of Singapore Savings Bonds (SSB) or are looking to invest in Singapore Savings Bonds (SSB), these are some tips to slightly maximize your returns.

Hack #1 – Switch To The Current Issue To Get More Interest

Compare the interest you are receiving for your investment to the interest in the current issue. If the interest rate is better, you can consider applying to the current issue and redeeming (selling) your previous investment to free up your capital. This allows you to get more interest with the same amount of investment.

Hack #2 – Apply For Singapore Savings Bonds (SSB) Nearer To The Application Deadline

The application period for Singapore Savings Bonds (SSB) opens for close to a month. There is no reason to apply at the start of the month as the application is not on a first-come-first-serve basis. As such, apply for the Singapore Savings Bonds (SSB) close to the application deadline and you can use the capital for other purposes such as getting more interest in your bank account.

Hack #3 – Get Monthly Income (Dividend) Using The Singapore Savings Bonds (SSB) Hack

Note that this only applies to DBS Multiplier Account.

If you have a DBS Multiplier account, you would know that there are certain criteria to meet to get a higher interest. To do so, one of the main criteria is to credit your income to your DBS Multiplier account. If you already have your income debited to another bank, you would be pleased to know that you can make use of the SSB hack to get an “income”.

Follow the step-by-step guide below to use Singapore Savings Bonds (SSB) to get “income” (dividend) so that you would be able to hit the criteria to get high interest with DBS Multiplier account.

Step 1: Ensure that your Central Depository (CDP) account has Direct Crediting Service (DCS) to your DBS Multiplier Account

During the opening of your Central Depository (CDP) account, you can set your Direct Crediting Service (DCS) to your DBS Multiplier account.

If you already have a Central Depository (CDP) account, you can log in to the SGX portal to change your Direct Crediting Service (DCS) to your DBS Multiplier account.

This means that the dividend from your Singapore Savings Bonds (SSB) investment will be credited directly to this account.

Step 2: Create a Singapore Savings Bonds (SSB) ladder whereby you apply for 6 consecutive Singapore Savings Bonds (SSB) issue

As mentioned earlier, Singapore Savings Bonds (SSB) payout the dividend from your investment every 6 months. If you apply for 6 consecutive Singapore Savings Bonds (SSB) issues, you will be able to receive dividends 12 times per year (once every month).

Step 3: Enjoy the monthly “income” (dividend) 6 months later

You will receive your first income (dividend) 6 months down the road from when you applied for it. Thereafter, you can expect an income (dividend) every month for the next 10 years until the holding period ends.

Step 4: Income (dividend) secured, time to spend with DBS

Now that the main criteria for having an income are settled, you can play around with other criteria to achieve higher interest with DBS Multiplier account.

Last Updated: 01 Jan 2025