Since I took a career break in Singapore, we have officially changed from a dual-income family to a single-income family in Singapore. It is a little daunting with the sudden loss in income and we had to be more cautious with our money. We are also a lot more interested in stretching our money further and thinking of ways to make our money last longer.

One of our current favourite fuss-free ways to get some spending money is to maximise our interest rate in savings accounts in Singapore. Most Singapore banks offer high-interest savings accounts to get you to transact more with them – invest, save, insurance, loan, etc. They are very easy to apply and you will receive the interest every month. Interest calculators are also available online and you can quickly calculate how much potential interest you will receive.

One of the common criteria of most high-interest savings accounts in Singapore is that they require you to credit your salary into the account to enjoy the higher interest. As a single-income family in Singapore, this means that we only have one account that will enjoy the higher interest rates as we are only receiving one salary.

We set out to review our bank accounts and what we can do to maximize our interest in our saving accounts to get the highest possible interest on a single account in Singapore. Usually high interest savings accounts in Singapore change their interests infrequently and you can basically auto-pilot them once you have set up the salary crediting, bills debiting etc.

The account that gets the salary

We usually only focus on the 3 local banks in Singapore, mainly because we tried a couple of foreign banks in the past, and we are not a fan of their Internet Banking experience. However, if are willing to consider foreign banks, they definitely offer great interest rates for their high interest saving accounts.

In our case, we choose to credit our salary to the OCBC 360 account. The reason is very simple, without any additional transactions, we will get 2% on the first $75k and 4% on the next $25k. UOB Bank and DBS Bank require you to do other transactions to get the higher interest even though we credit our salary. This makes it slightly more complicated, which we are not a fan of.

If you are willing to go a step further, you can also get a further 1.2% on the first $75k and 2.4% on the next $25k if you grow your account by $500 per month. If you are crediting your salary to this account, this criteria is relatively easy to hit.

The account that gets the dividend

We do not have a lot of investment as we are a lot more risk-adverse due to the arrival of our little peanut. Usually, fixed deposits and Singapore Saving Bonds (SSB) are our favourite type of investment as they are almost risk-free and do not require a lot of active management.

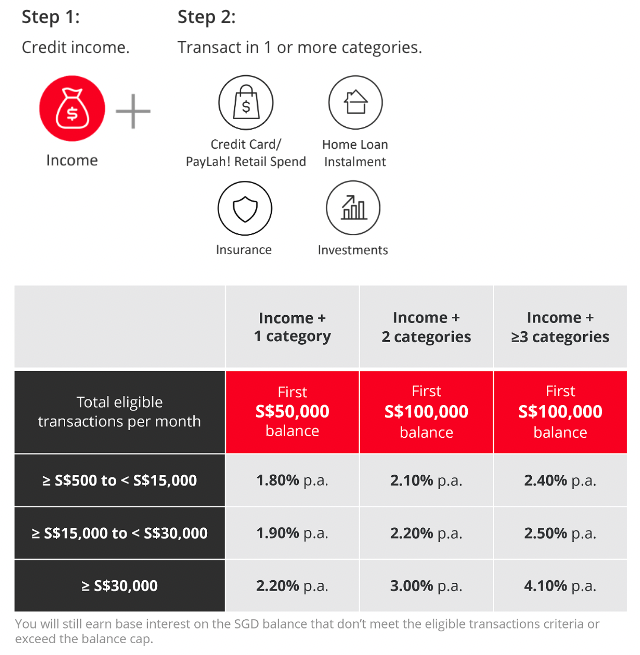

We raved about this hack multiple times, but building a “SSB ladder” and crediting the dividend to our DBS Multiplier account helps us to create another “income”. With this hack, you can earn up to 2.4% on up to $100k balance if you have at least $500 in total transactions.

It is relatively easy to hit the transaction in the “credit card / paylah! spending” as DBS does not have any requirement on the minimum spending, and simply adds up the total transaction made across the categories and credited income to decide on the interest earned.

The account that gets the bill

Like any Singapore household, we also have a ton of household bills to pay – utilities, internet, mobile, maintenance fees, and so on. We usually consolidate our bill payments to allow payment from one account. This makes our lives infinitely easier and makes it so much easier to keep track of missed payments.

We use the UOB One account to pay all of our bills, both via GIRO and via the credit card options. You can get higher interest with the UOB One account if you make 3 GIRO debit transactions and spend at least $500 using a UOB credit card. You can earn an interest of up to 4% based on your monthly balance and the maximum effective interest rate you can get is 3% on a maximum $75k balance.

Just by paying our bills using the UOB One account, we managed to meet the criteria to get the higher interest rates. The little trick here is to use GIRO to pay off the smaller bills and use the credit card to pay the bigger bills. The payment using the credit card will go towards hitting the $500 credit card spending.

Interest rate summary

On a single income in Singapore, we managed to snag pretty good interest on all 3 of the local banks’ higher interest saving accounts. While it took a little initial work to plan the transactions and set up the necessary instructions in the respective banks, it was a one-time effort (or at least until they change their criteria again).

The fact that the local banks’s Internet Banking interface is really easy to use, and most (if not all) transactions can be done online makes it so much easier to manage. We love the fact that the interest for high interest saving accounts is calculated on a monthly basis. It’s definitely satisfying to see our interest being credited into our bank account at the start of every month.

Last Updated: 31 Mar 2024