It is many people’s dream to be able to own many properties in their lifetime and be a bao zhu po. Just think, if you have at least 2 properties, you can stay in 1 and rent 1 out to collect rent for a living.

In Singapore, about 90% of the residents own an HDB flat. As all of us know, by owning an HDB flat which is subsided housing in nature, we accepted many clauses that HDB enforces. This can include not being allowed to keep large dogs and not being able to rent out your house for less than 6 months.

Private property, on the other hand, is seen as a good investment vehicle in land-scare Singapore which can yield both good rental rates and an increase in appreciation value. Even if the economy goes south, they still have a physical property to look and hold on to. Hence, it is an investment form that many wants to add to their portfolio.

Now, the big question everyone always have in their mind is:

Can I still buy a private property while owning a HDB?

It’s a resounding YES! You can own a HDB and private property concurrently, as long as you fulfil the following requirements.

Basic Requirements

Fulfilling Minimum Occupation Period (MOP)

MOP is the number of years the HDB / EC owners need to occupy the flat before they are allowed to do further housing actions. This can include selling the flat, subletting the entire flat, or buying a new unit. Currently, the MOP is set at 5 years.

MOP is calculated from the date the owners collected the keys to their flat. If you have rented the entire flat due to special circumstances or have infringed the flat lease, that period is not considered in the MOP.

I’ve Fulfilled the MOP. What’s Next?

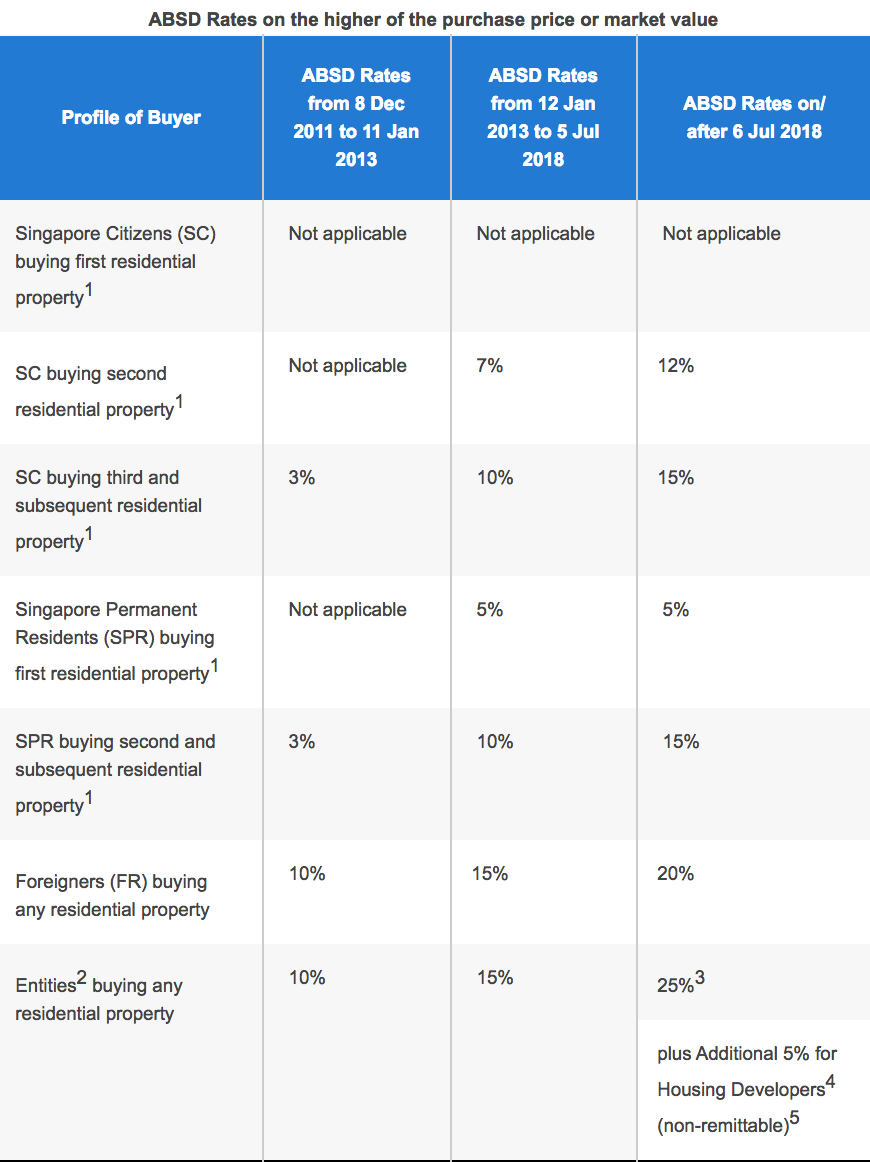

Additional Buyer Stamp Duty (ABSD)

If you are looking to purchase a private property as a second property, you will have to pay additional buyer taxes. The ABSD for the 2nd property is 12% and the 3rd and subsequent property is 15%. This is on top of the normal buyer stamp duty that is payable for the purchase of any property.

For a $1 million private property, the total stamp duty that you need to pay would be roughly $145k.

Home Loans and More

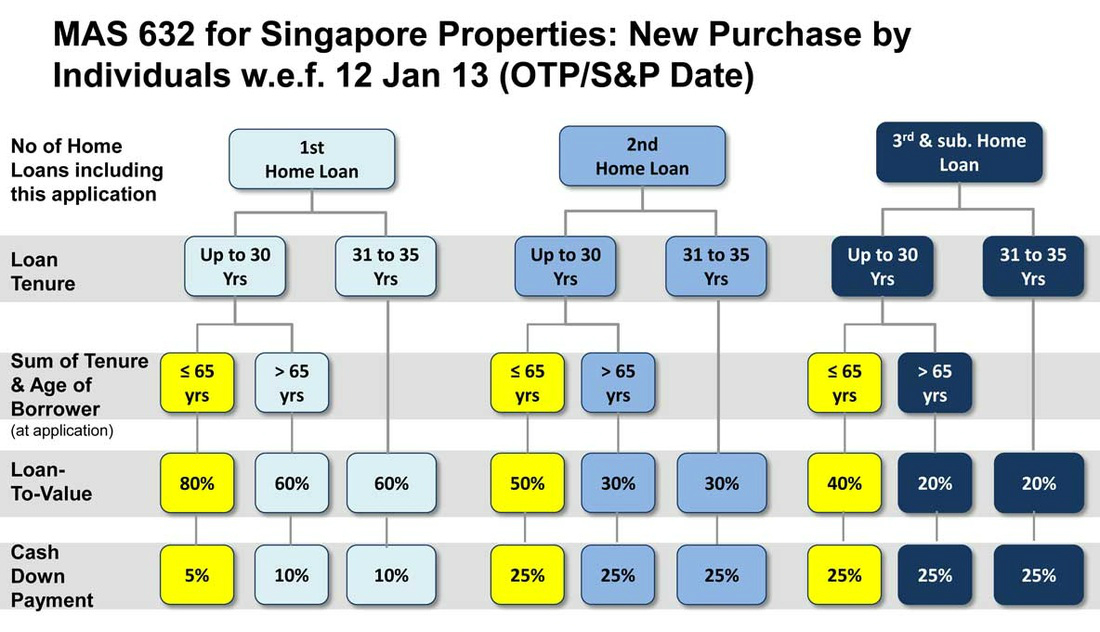

There is always a misconception by many that you need to pay off your first loan before you can get another loan. This is not true. You can always get a second loan, or even a third loan and more, subject to certain conditions.

Loan-to-Value Ratio (LTV)

These conditions will affect the loan-to-value ratio (LTV ratio), which will determine the amount you can loan from the bank, calculated as a percentage of the property value price or purchase price, whichever is lower.

Loan Tenure

For HDB loans, the maximum loan tenure has been shortened from 30 years to 25 years since 2013. On the other hand, a bank loan can go up a maximum tenure of 35 years. Generally, loan tenure above 30 years will result in a lower LTV ratio.

Sum of Tenure and Borrower Age

Once you are above 35 years old, the LTV ratio will be reduced greatly as the risk of lending is much higher.

Total Debt Servicing Ratio(TDSR)

The total debt servicing ratio (TDSR) is the ratio of loan you can borrow as a percentage of your income. Currently, TDSR is set to 60% of your monthly income. The loan refers to a collective monthly repayment of your credit card, housing, personal, car loans, and so on.

So, how will this affect your loan for your second property?

Example

If you and your spouse are earning $10,000 per month, and have a collective monthly debt of $4000, you only can use up to $2000 for your monthly repayment of your second property as the TDSR threshold is $6,000 ($10,000 * 60%)

Usage of CPF

If you have used your CPF in your first property, you cannot use CPF for your second property unless you have set aside the basic retirement sum (BRS) in your CPF account. Currently, the BRS is set at $80,500, and your Special Account(SA)(including investments) and Ordinary Account(OA) can be used to contribute to this amount. Thereafter, the excess can be used for the repayment of your second property, up to the valuation limit.

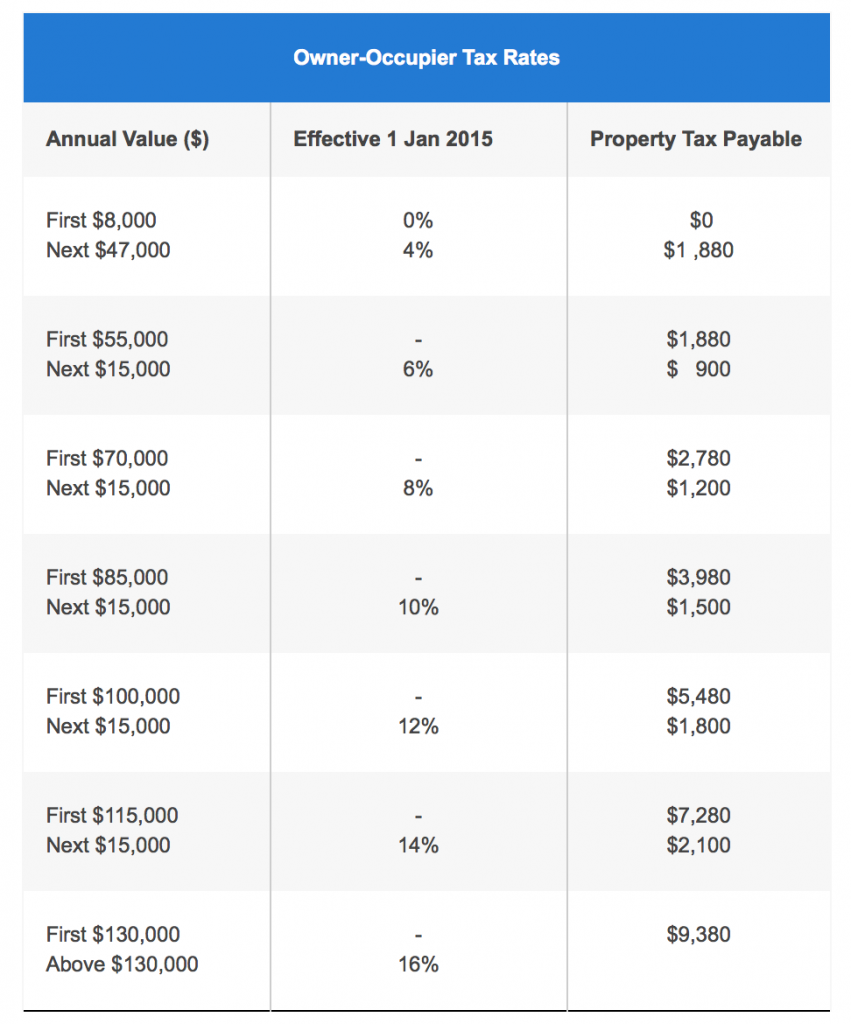

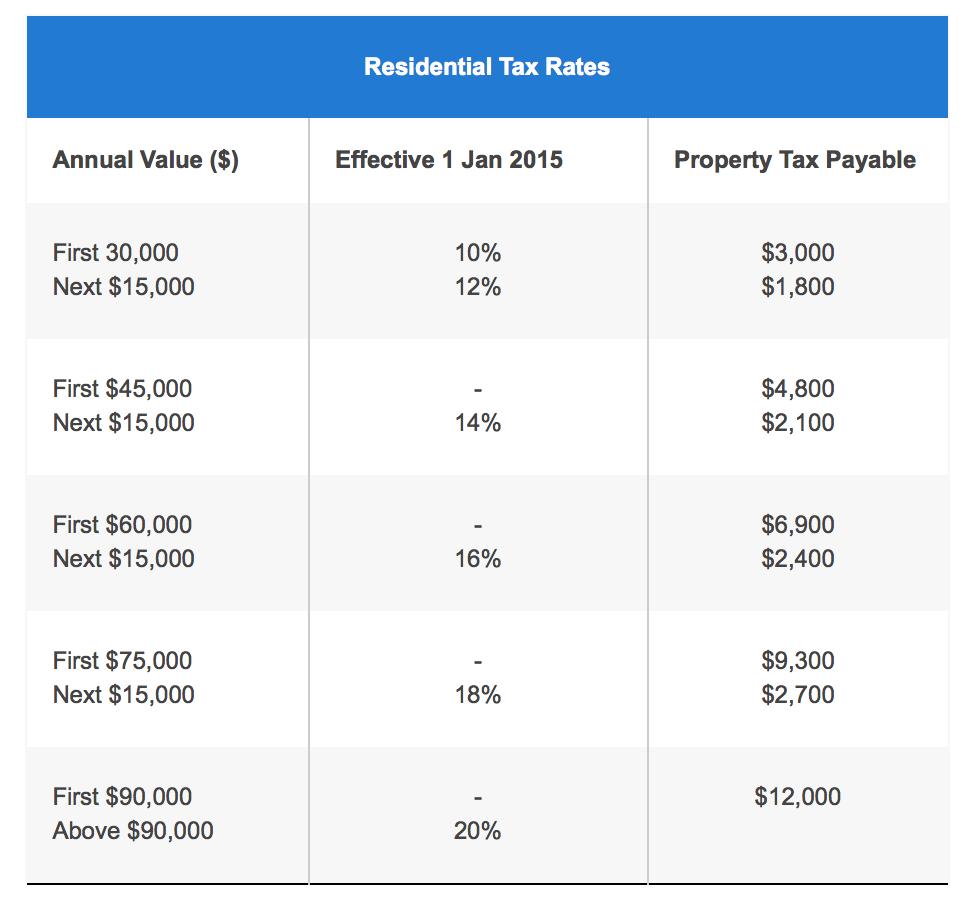

Property Taxes

When you are renting out your property as a source of income, the property tax you are paying for that property will be higher.

Tax Differences

Assuming that your property’s annual value is $30,000, the property tax for:

Owner-Occupied = $880

Residential = $3000

Don’t forget that the income generated from renting your property is subject to income tax.

Final Words

While you can legally purchase a private property after fulfilling the 5 years MOP of your HDB flat, it is important that you exercise financial prudence in managing your finances as there are a lot of additional expenses that comes with the second property purchase.

Last Updated: 13 Nov 2018