Buying an HDB BTO together with your partner signifies commitment with each other, but it also implies potential debt for the next 20 to 25 years. But how much does an HDB really costs, and how much do we need to fork out for the downpayment?

Trying to make sense of the information on HDB’s website is a lot of hard work! Hence, we have done all the hard work and create this guide especially for you. In this guide, you will know how to calculate the total costs an HDB BTO and the amount you have to fork out at each stage of purchase.

Application Period

Application Fee

Whenever you want to apply for any BTO/SOBF (build to order/sales of balance flats) sales launch, you will need to pay a non-refundable $10. This is not payable from your CPF, and should you decide to change your choice of area/number of rooms applied, you will have to make the payment again.

Damage = $10 x n times ( n = the number of times you paid)

First Appointment (Registration and Flat Selection)

Option Fee

Lady luck shines on you, and you get a queue number to select your BTO / SOBF, you will need to pay an option fee on the first appointment (registration and flat selection). The option fee acts as an option to purchase (OTP) and reserve your rights to purchase the flat. Note that this is non-refundable should you decide to back out of the purchase subsequently.

The amount varies based on the HDB flat types, and goes into your downpayment should you be taking a bank loan or you do not have sufficient money in your CPF OA (ordinary account) for an HDB loan. You can also opt for it to be reimbursed in cash. The amount is as follows:

| Option Fee | |

| 4/5 Room and Executive Flat | $ 2,000.00 |

| 3 Room | $ 1,000.00 |

| 2 Room | $ 500.00 |

Damage = respective option fee

Option fee can be paid in either cash, NETS, or Credit Card during the first appointment.

AHG / SHG (Additional CPF Housing Grant / Special CPF Housing Grant) (If Applicable)

If you are eligible for grants, that’s great! It will ease quite a substantial amount of financial burden, and potentially reduces a large amount of debt. There are 2 different grants that the government gives – AHG and SHG. What’s the difference?

- You cannot get AHG if your income more than $5000. However, for SHG, the income cap is at $8500.

- If you are getting a flat in a mature estate, you cannot get AHG.

- If you are getting a 5 room flat in non-mature estates, you cannot get SHG. SHG only applies for 2 room flexi, 3 room, and 4 room flat in non-mature estates.

Things to note:

You need to note that AHG and SHG are given only if at least 1 of the applicants (not occupier) has been employed for at least 1 year continuously. The 1-year employment is taken such that if you are applying for a Feb 2017 BTO, the 12 months included in the computation is from Feb 2016 to Jan 2017. HDB is extremely strict on these criteria, and appeals may not be entertained. (Do comment below if you have successfully gotten grants despite not fulfilling the criteria!)

Both grants are calculated based on the average total household income between the couple/family. This means that you add up the past 1-year salary of everyone staying in the house (yes, occupier included) and divide it by 12. And yes, the 12 months included in the calculation is from Feb 2016 to Jan 2017 if you are applying for a Feb 2017 BTO. Note that you do not divide the average monthly income by the number of people staying as it is asking for average monthly household income.

Grant Breakdown Chart

The breakdown of grant at each income tier is as follows:

| Average Monthly Household Income | AHG | SHG |

| $1500 and less | $ 40,000.00 | $ 40,000.00 |

| $1501 – $2000 | $ 35,000.00 | $ 40,000.00 |

| $2001 – $2500 | $ 30,000.00 | $ 40,000.00 |

| $2501 – $3000 | $ 25,000.00 | $ 40,000.00 |

| $3001 – $3500 | $ 20,000.00 | $ 40,000.00 |

| $3501 – $4000 | $ 15,000.00 | $ 40,000.00 |

| $4001 – $4500 | $ 10,000.00 | $ 40,000.00 |

| $4501 – $5000 | $ 5,000.00 | $ 40,000.00 |

| $5001 – $5500 | $ – | $ 35,000.00 |

| $5501 – $6000 | $ – | $ 30,000.00 |

| $6001 – $6500 | $ – | $ 25,000.00 |

| $6501 – $7000 | $ – | $ 20,000.00 |

| $7001 – $7500 | $ – | $ 15,000.00 |

| $7501 – $8000 | $ – | $ 10,000.00 |

| $8001 – $8500 | $ – | $ 5,000.00 |

Do note that this grant cannot be used for the cash part of the downpayment (if any) for your flat. However, it can be used for the CPF portion of the flat, including using it to offset the downpayment. However, you need to note that the disbursement of the grants may not happen before the downpayment is due. Hence, you will need to ensure that you have sufficient money in your CPF OA or cash on hand.

Damage = negative (SHG + AHG) OR 0(zero) (if you can’t get any grant)

Second Appointment (Signing of Agreement for Lease)

Downpayment

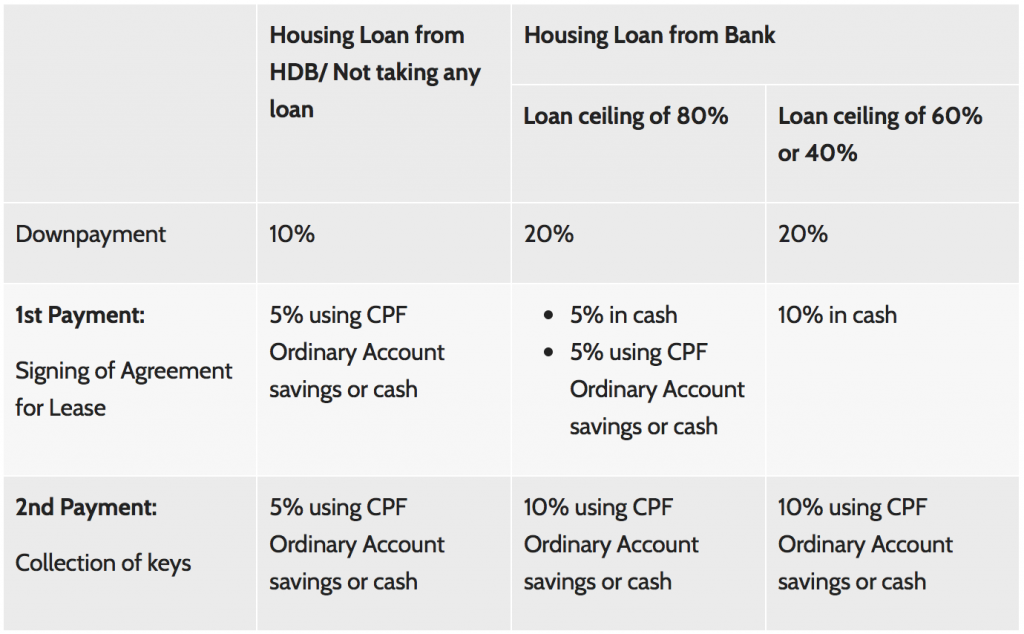

You will be called for the second appointment, usually within 4 months of the first appointment. In this appointment, you must be mentally and financially prepared that you will need to pay the downpayment for your flat. If you are taking a bank loan, the downpayment required is 20%. Otherwise, it will be 10% if you are taking an HDB loan. If you fall under the below 2 conditions, you are eligible for the staggered downpayment.

- First-time couple, where 1 of them is younger than 30 years old (based on birthday)

- Existing flat owners, who brought an uncompleted 2-room or 3-room flat in a non-mature estate, and have yet to legally sold their existing flats

Staggered downpayment meant that you can pay the first half of downpayment in the second appointment and the rest in the third(last) appointment. The current staggered downpayment rates for each type of loan is as follows:

If you have gotten any CPF grant, you can use it to offset the payment as necessary and top-up the remaining. Note that if HDB requires you to pay in cash ONLY, the grant cannot be used.

Damage = downpayment

Stamp Duty

Stamp duty is a lump sum tax that you need to pay whenever you purchase or sell your property. It is calculated based on the value of the property and the percentage is as follows:

| Calculation of Stamp Duty | |

| First $180,000 | 1% |

| Second $180,000 | 2% |

| Thereafter | 3% |

This amount can be payable via CPF.

Damage = (n * 3%) – 5400 , where n = the purchase value

In addition, if your annual Service & Conservancy Charges (S&CC) and an annual rent of $1 adds up to more than $1000, you will need to pay annual stamp duty for the year.

It is calculated as:

Damage = S&CC * 4 * 0.4% (only if applicable)

Conveyancing Fee

Conveyancing fee is legal fees payable if HDB handles the purchase of your property and/or provides you an HDB housing loan. If you are borrowing from banks, an additional conveyancing fee is also payable to the bank.

| Calculation of Conveyancing Fee | |

| First $30,000 | $0.90 per $1,000 |

| Second $30,000 | $0.72 per $1,000 |

| Thereafter | $0.60 per $1,000 |

Similarly, this can be payable via CPF. If your conveyancing fee cost less than $20, you would still have to pay the minimum amount of $20.

Damage = (maximum of n, cap at 30,000) / 1000 * 0.90 + (maximum of n – 30,000, cap at 30,000) / 1000 * 0.72 + (maximum of n – 60,000) / 1000* 0.60 , where n = the purchase value

Caveat Registration Fee

A caveat registration fee is payable to give notice of your interest in the flat pending the Lease Registration with the Singapore Land Authority to protect your interest in the flat. It is a flat rate of $64.45 and similarly, can be payable by CPF.

Damage = $64.45

Third and Last Appointment (Collection of Keys)

Finally, you have reached the final lap of your flat purchase, and you are called down to collect your keys!

Registration Fees

There are 2 types of registration fees – lease in-escrow registration fee, and mortgage in-escrow registration fee. Lease in-escrow registration fee is payable if HDB is acting for you in the flat purchase. This fee is compulsory if you are purchasing a BTO / SOBF flat. Whereas for mortgage in-escrow registration fee, it will only be payable if you are taking a housing loan from a bank. These 2 registration fees can be paid via CPF.

Damage = $38.30 + $38.30(only if taking a bank loan)

Survey Fee

The survey fee is payable based on the types of flat and is to offset costs of engaging professional surveyors. The rates shown below are before GST and are similarly payable via CPF.

| Flat Type | Survey Fee |

| 1 Room | $ 150.00 |

| 2 Room | $ 150.00 |

| 3 Room | $ 212.50 |

| 4 Room | $ 275.00 |

| 5 Room | $ 325.00 |

| Executive Flat | $ 375.00 |

Damage = survey fee * 1.07

Stamp Duty on Deed of Assignment

This stamp duty on Deed of Assignment is payable if you are taking a loan from a bank. It is also payable using CPF.

Damage = bank loan * 0.4% , cap at $500 (only if taking a bank loan)

Additional Payments

Home Protection Scheme (HPS)

For those who are using your CPF OA account to pay for your installments, you are required to opt-in for the HPS. This is a mortgage-reducing insurance scheme by the CPF Board where, in the event of permanent disability or death before the insured person turns 65, the CPF Board will pay the outstanding housing loan amount, based on the amount insured under HPS.

The premium amount is dependent on factors such as your declared percentage of coverage, loan amount, age, and gender and can be paid using CPF, on an annual basis.

The HPS calculator can be found here.

Fire Insurance

If you are taking an HDB loan, you would also need to purchase fire insurance from HDB appointed agent – Etiqa Insurance. You will need to produce a valid Certificate of Insurance on the collection of flat keys and cannot be paid using CPF. The 5 years premium is as follows:

| Fire Insurance | ||

| Flat Type | 5 years Premium(Including GST) | Billing Sum Insured |

| 1 Room | $ 1.50 | $ 19,300.00 |

| 2 Room | $ 2.50 | $ 26,300.00 |

| 3 Room | $ 4.50 | $ 41,800.00 |

| 4 Room | $ 5.50 | $ 69,100.00 |

| 5 Room | $ 6.60 | $ 75,600.00 |

| Executive/Multi Generation | $ 7.50 | $ 98,200.00 |

| Studio Apartment (Type A) | $ 3.50 | $ 29,000.00 |

| Studio Apartment (Type B) | $ 4.00 | $ 37,200.00 |

Service & Conservancy Charges (S&CC)

S&CC are paid on a monthly basis and need to be paid before key collection. This cannot be paid via CPF. The charges varied for different room types of flats and the region you are living in.

**note that any fees that is payable via CPF can also be paid with cash, if there is insufficient amount in your OA account.

Monthly Installments

The remaining amount can be loaned from the bank or HDB Board after deducting the grants given and downpayment paid. If you have existing CPF OA or excess cash on hand, you can choose to make partial payments to reduce your mortgage amount. Thereafter, you will need to choose the period of loan for monthly installments.

As we all know, loans come with interest. Hence, the shorter your loan period, the lower the interest amount you paid, and the lower your loan amount, the lower the interest amount you paid. The official calculator can be found here. The maximum loan period for an HDB loan is 25 years.

Sample Calculation

In this sample, we will be looking at a $300,000 4-room flat in a non-mature estate.

We can assume the following:

- At least one of them has worked for at least 1 year consecutively, and are hence, eligible for the grant.

- Combined income is $7000 per month, which means HDB grant totals to $20,000.

- Loan is borrowed from HDB at 2.6% per annum for the maximum tenure of 25 years. (assume interest rate don’t change)

Calculation as follows:

Application Fee = $10 (cash) (The couple receive a queue number at their first try)

First appointment

Option Fee = $2,000 (cash) (refundable)

AHG / SHG = -$20,000 (deposited to CPF)

Second Appointment

Downpayment = 15,000 (CPF)

Stamp Duty = 4,200 (CPF)

Conveyancing Fee = $206.08 (CPF)

Caveat Registration Fee = $64.45 (CPF)

Total = $19,470.53

Third Appointment

Downpayment = 15,000 (CPF)

Registration Fee = $38.30 (CPF)

Survey Fee = $275 (CPF)

HPS = $140.53 (Cash)

Fire Insurance = $5.50 (Cash)

Conservancy Fees = $74.50 (Cash)

Total = 15.533.83

Monthly Installments

Assumption

- The grant is used to offset their loan amount

- Their final loan would be $250,000.

| Loan Period | Monthly Installment | Total Amount Paid | Interest Paid |

| 25 | $1135 | $340,500 | $90,500 |

| 20 | $1337 | $320,880 | $70,880 |

| 15 | $1679 | $302,220 | $52,220 |

At 25 years of loan tenure, the total amount paid for the loan is $340,500.

The above calculations only include the monthly housing installments and do not include monthly bills such as utility bills, S&CC, property taxes, etc.

How much does a HDB BTO really cost?

Hence, to answer the topic of this article “How much does a HDB BTO really cost?”, the answer is

$10 + $19,470.53 + $15,533.30 + $340,500 (flat price after downpayment) = $375,513.83

That’s it! These are the amount you have to prepare at each stage of the appointment and every month. While we see that the flat value is $300,000, it might not actually be the case as we need to bear legal costs, interest costs, and other ad hoc costs.

Do calculate your finances carefully before you decide to BTO / SOBF for HDB flats. Especially for SOBF flats where the timeline is tighter, and you might need to plan your finances together with weddings, renovations, cars, and even babies.

If your finances allow, you could also consider getting an EC. Do check out our guide on how must an EC costs.

Last Updated: 13 Oct 2018