According to a global ranking , Singapore has the 2nd most expensive housing market in the world. If you are staying in or owning a condo in Singapore, it is a big deal. It is especially so if you are staying in one that is near the city area or in the city area.

If so, how much do you actually have to earn per month to be able to afford one? In this article, we will explore the monthly income that you would have to earn in order to afford the bragging rights.

How much must you earn to afford a private condo?

Assumptions made:

- Owner age are less than 35 years old, which means that the loan tenure is the maximum of 30 years.

- Owner do not have any prior debt or financial commitment.

- Monthly instalments is calculated using an interest rate of 3.5%, which is the recommended rate from MAS to calculate instalments amount.

- Income remains constant for the entirety of the duration.

- Maximum loan amount taken based on their income in order to reduce the initial cash outlay for the purchase.

- Standard 3 bedder of approx 1000 sqft apartment used for calculation.

- New sale condo used for consideration.

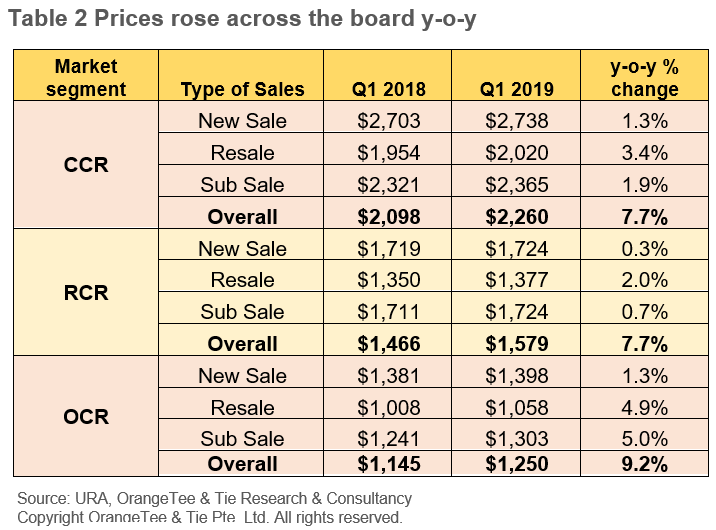

We will be using the Q1 2019 average psf price for each region based on a research done by OrangeTee.

OCR [Outside Central Region]

The PSF of a new launch OCR condo is $1359 psf in the Q1 of 2019. Given that we are looking for a reasonable size of 1000 sqft to live comfortably, the approx price range we are looking at is $1.359M.

For private condos, the maximum that can be borrowed from the bank is 75% of the unit value.

maximum amount : 1.359M * 75% = 1.019M

For private housing, the maximum amount that the owner can borrow is up to a maximum of 60%, due to the total debt servicing ratio (TDSR).

Based on the above chart, the minimum income required is slightly below $8K, roughly $7625 to be more exact. The monthly instalment is $4580.

The initial outlay required is the 25% downpayment would be $340k, $39k for stamp duty and $2500 for lawyer fees. These only include the big ticket payment and does not include the miscellaneous fees that you need to fork out here and there.

This means that other than earning a minimum income of $7625 per month, you will need to also have a savings of at least $382k.

RCR [Rest of Central Region]

The PSF of a new launch RCR condo is $1724 psf in the Q1 of 2019. Given that we are looking for a reasonable size of 1000 sqft to live comfortably, the approx price range we are looking at is $1.724M.

For private condos, the maximum that can be borrowed from the bank is 75% of the unit value.

maximum amount : 1.724M * 75% = 1.293M

For private housing, the maximum amount that the owner can borrow is up to a maximum of 60%, due to the total debt servicing ratio (TDSR).

Based on the above chart, the minimum income required is above $9k, roughly $9680 to be more exact. The monthly instalment is $5810.

The initial outlay required is the 25% downpayment would be $431k, $54k for stamp duty and $2500 for lawyer fees. These only include the big ticket payment and does not include the miscellaneous fees that you need to fork out here and there.

This means that other than earning a minimum income of $9680 per month, you will need to also have a savings of at least $488k.

CCR [Core Central Region]

The PSF of a new launch CCR condo is $2738 psf in the Q1 of 2019. Given that we are looking for a reasonable size of 1000 sqft to live comfortably, the approx price range we are looking at is $2.738M.

For private condos, the maximum that can be borrowed from the bank is 75% of the unit value.

maximum amount : 2.738M * 75% = 2.053M

For private housing, the maximum amount that the owner can borrow is up to a maximum of 60%, due to the total debt servicing ratio (TDSR).

Based on the above chart, the minimum income required is slightly below $16k, roughly $15,370 to be more exact. The monthly instalment is $9220.

The initial outlay required is the 25% downpayment would be $685k, $95k for stamp duty and $2500 for lawyer fees. These only include the big ticket payment and does not include the miscellaneous fees that you need to fork out here and there.

This means that other than earning a minimum income of $15,370 per month, you will need to also have a savings of at least $783k.

Do note that this is an estimated figures that help you with your initial financial plans, and does not represent the actual values. You will need to refer to the respective banks for actual loan amounts.

What is the maximum condo price can you afford?

Bonus tips! You can also use the below steps to calculate the maximum condo price that you can afford based on your salary.

- Calculate the total salary.

- Monthly Instalment = Calculate salary *60% (The maximum instalments you can pay per month is 60% of your salary. )

- Total Loan = Monthly Instalment * 360 (The maximum loan period is 30 years)

- Maximum Condo Price = Maximum loan * 0.815 (Assuming loan interest = 3.5%)

Do note that this is an estimated figures that help you with your initial financial plans, and does not represent the actual values. You will need to refer to your respective property agents for advice.

Last words

Interestingly, the income you need to earn to purchase a condo is actually lower than if you were to buy an EC. The main reason being that housing loans for private condos allow you to have a total debt/loan of up to 60% of your total income. Whereas for EC, you are only allowed to use up to 30% of your income for debts/loans.

Bear in mind that this will actually reduce your disposable income significantly if you choose to max out the full 60% allowance for housing loan.

| Region | Monthly Income |

| OCR | $7625 |

| RCR | $9680 |

| CCR | $15,370 |

For a better comparison, do check out our guide on how much income you should have if you want to buy an EC, now updated to the 2020 edition.