Continuing our previous post, How Much Can You Receive in Cash and CPF Once You Sell Your HDB?, does anything change if you are above 55 years old? What will happen to your CPF if you sell your HDB? Can you purchase another flat using your CPF once you sell your existing HDB?

Let’s have a walk through scenario.

- You and your spouse are 57 years old at the year of 2020

- You have a resale 4-room flat that you brought in the 90s for $200,000

- You and your spouse are both listed as owner of the HDB

- You received a $40,000 CPF housing grant for the unit, which is used during the downpayment and to reduce the mortgage loan

- You took up a 25-years HDB loan with an interest rate of 2.6%

- Instalments are fully paid using CPF

- You have just fully paid off your HDB loan

- You spent $30,000 on renovation

- Market price for your flat is $350,000

What will happen?

You have now retired and enjoying your golden years. Currently, you are looking to perhaps downgrade to a smaller unit or maybe, looking to get a house nearer to your children.

How will the sales proceed from selling your HDB be allocated now that you have an additional account called a “Retirement Account (RA)” sitting in your CPF?

Step 1: Calculate the actual “take-home price” from selling your HDB.

Assuming that you have hired a property agent to settle the sales of your HDB, the commission of about 2% of the selling price works out to about $7,000.

Agent Fee = $7,000

Take-Home Price = $343,000

Step 2: Redeem your HDB loan

You have no more outstanding HDB loan.

Step 3: Pay back principal amount + accrued interest of CPF taken (CPF grant included)

Over the past 25 years, you have been paying for the instalments using your CPF. If you were to sell your house, it would be expected that the proceeds will go back to your CPF first to payback the outstanding amount.

You can login to the CPF portal to view the actual CPF amount you have used, both principal and accrued interest.

You would have taken an initial loan of $160,000 after deducting the grant of $40,000. Over the loan tenure of 25 years, you would have used a total of $218,000 from your CPF. Along with the grant of $40,000 given at the start of the purchase, the total amount to return to CPF, including accrued interest amounts to $384,000.

Take-Home Price = -$41,000

What does a negative value means?! Do I need to top up CPF with my own monies?!

Well, according to the CPF website, if the selling price of your HDB is not sufficient to cover the principal amount + accrued interest, you do not need to top up the shortfall in cash, as long as the property is sold at market value.

In this scenario, we assumed that you have sold the HDB at market price, which means that you do not need to fork out additional cash from your own pocket.

Step 4: Calculate the actual “overall cost” you fork out for the purchase of your HDB. (Yes, that includes your renovation as well.)

In your initial purchase, there are a couple of large fees that you pay for, which does not goes toward paying off the house. They are mainly the stamp duty and the renovation costs.

Stamp Duty = $2,200

Renovation = $ 30,000

Take-Home Price = -$32,200

Step 5: Calculate any “refunds” from your CPF

The payback to CPF is then used to top up the retirement account (RA) of you and your spouse to the full retirement sum (FRS). If there are any balance, you will get them in cash.

In this scenario, both you and your spouse have a FRS of $171,000. We will assume that your current RA is empty for easy calculation. This means that of the $343,000 payback to CPF, you would get back $1000 in cash.

Take-Home Price = -$31,200

Summary of Returns

In summary, this is the amount of cash and CPF you would receive after selling your property.

| CPF | $342,000 |

| Cash | -$31,200 |

Any proceeds that you received from selling your flat are unfortunately, returned to your CPF as you have used them. Only after maxing out the RA account, will the excess be refunded to you.

Any cash you have used to pay the stamp duty and renovations are unfortunately sunk costs, and can’t be recovered. On the bright side, the renovations done 25 years ago have probably reached their maximum potential.

What are your options?

Now that you have sold your flat, what are your best bet?

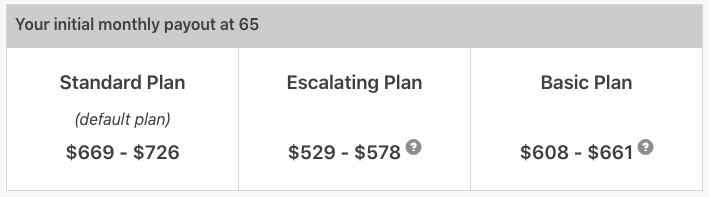

Option 1: Do nothing!

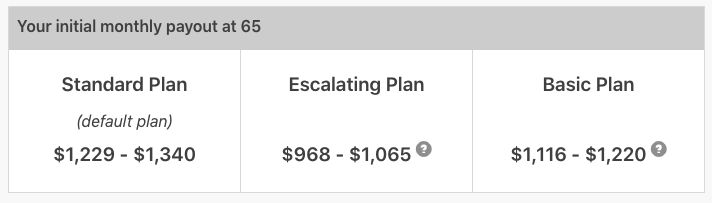

If you choose not to get another flat, and instead, move in with your children, the amount in your RA will continue to roll in interest until it is time for you to withdraw them under the CPF Life when you have hit 65 years old.

The expected monthly payout for you and your spouse would be:

Male:

Female:

Option 2: Get a Resale 3-Room HDB

If you are looking to downsize into a smaller unit, how will the cashflow go? Do you need to top up additional cash, or can you use your CPF for the purchase?

A quick scenario. Let’s say you would like to get a resale 3-room HDB flat at $200,000. As you and your spouse are no longer working, you are unable to get a home loan, and would have to pay for the house upfront.

As long as the house can last you till at least you are 95 years old, you are able to use CPF to fund your purchase. The maximum amount you can use from CPF is any amount in your RA above the basic retirement sum (BRS). This means that both you and your spouse can use $85,500 each to fund this property, which comes up to a total of $171,000 payable from CPF.

For the remaining outstanding of $29,000, you would need to use cash to top up the difference.

With the large payment, mainly stamp duty and renovations of $40,000, be prepared to fork out about $72,000 in cash for this purchase.

| CPF | $171,000 |

| Cash | $72,000 |

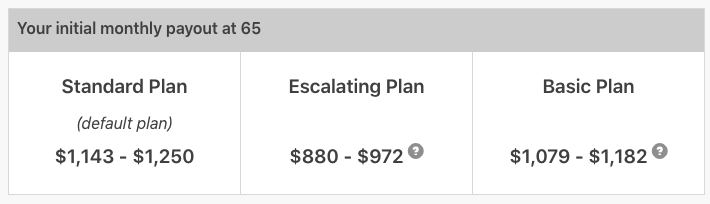

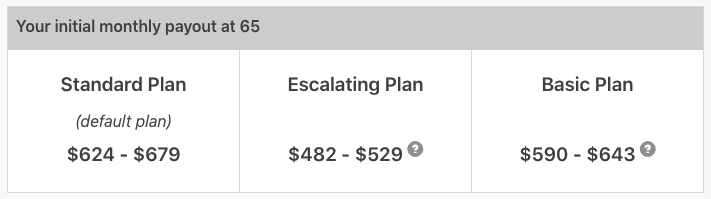

You would also be able to receive the monthly payout under CPF Life upon reaching 65 years old based on your BRS.

Male:

Female:

Last Words

Many people in their 50s and 60s are hesitant to sell their flat in their golden age as they are worried of “locking in” their sales proceeds in their CPF. This is primarily due to many using their CPF to pay for the flat.

In any way, selling your house when you are 55 years old should always be a prudent decision to make. This is especially so when you are no longer working, and are relying on the flat as the main source of income. If you are not interested in selling your flat, you can also consider the lease buyback scheme, or downgrading to a 2-room flexi flat that is designed with the elderly in mind.